Follow the Credit System Step-by-Step

Why Your Credit Score Dropped for No Reason (Hidden Patterns Explained)

Your credit score can drop suddenly even when you pay on time. Discover the hidden timing patterns, original system insights, and practical steps to understand and recover from unexpected drops.

CreditPatterns.com

3/31/20266 min read

You open your credit score app one morning and see a drop of 20, 30, or even 40 points. No late payments. No new cards. No big purchases. Just… a drop.

This exact moment has happened to millions of people and almost always feels like it came out of nowhere — especially when it hits right before a mortgage application, car loan, or apartment approval.

The truth is these “random” drops are rarely random. They follow predictable patterns most people never see until it’s too late.

This is how credit scoring works as a system—not isolated factors, but patterns interacting over time.

Unlike most articles that blame “high utilization” or “a new card” and stop there, this piece reveals the hidden timing patterns and system-level dynamics that actually cause sudden score drops — and what you can do when they happen.

A sudden credit score drop with no obvious reason usually stems from monthly reporting cycles, statement closing dates, small shifts in reported balances, or new account aging effects. These drops are often temporary, with noticeable recovery beginning in 30–90 days if your underlying payment behavior stays strong.

Here’s where it gets confusing: you can pay every bill on time and still see a drop because the system doesn’t see your real-life behavior — it sees monthly snapshots and how those snapshots compare to your recent history.

The underlying system cause is that credit scoring models are constantly re-evaluating risk based on the most recent data they receive. The visible trigger is almost always a monthly reporting cycle from one or more creditors.

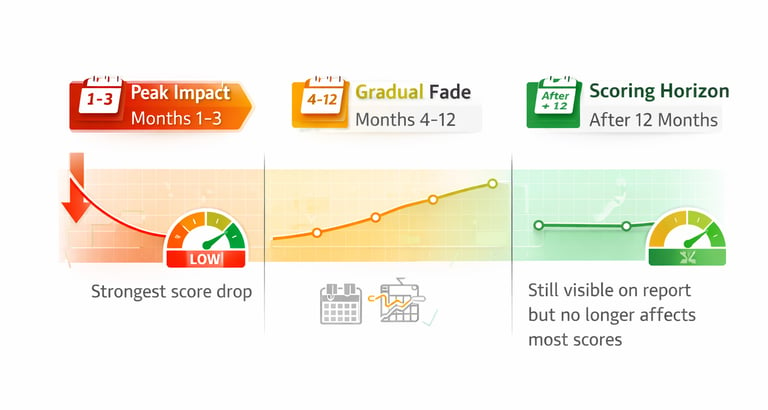

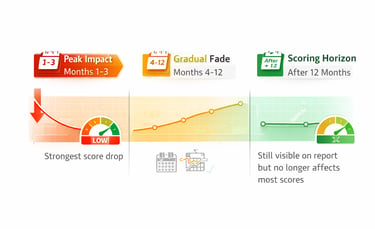

Score impact registers within days of a creditor reporting updated information (typically once per month on or near your statement closing date) because models recalculate using the freshest data available. The strongest negative weight occurs in the first 1–3 months, then gradually fades. Most models stop factoring the change after approximately 12 months. Recovery accelerates when time passes alongside consistent positive behaviors such as on-time payments and stable or improving utilization.

This ties directly into why your credit score changes, where we explore the monthly rhythm of credit data.

At their core, sudden score drops are driven by a set of interconnected patterns that together form one unified mental model of how the credit system reinterprets your file each month.

Statement Snapshot Effect occurs when your score reacts to the exact balance reported on your statement closing date. Even if you pay in full later that month, the reported snapshot can push utilization higher and trigger a drop.

Utilization Creep Pattern happens when small, gradual increases in reported balances push your utilization ratio higher without you noticing. This pattern often combines with statement timing to create sudden, unexpected drops.

New Account Aging Drag pulls down your average age of accounts while the positive payment history on the new account hasn’t had time to build depth. This effect is strongest in the first 3–6 months after opening a new account.

Reporting Lag Surprise occurs when a creditor reports old or delayed information, causing a sudden recalculation that feels completely random.

Here’s how all these patterns work together as one system: Your credit score doesn’t drop because you did something wrong. It drops because the system reinterprets the latest monthly snapshots through the lens of recency, utilization, and age. The patterns don’t act alone — they amplify or dampen each other depending on timing. Understanding this interconnected view turns “random” drops into predictable signals you can manage.

Elena in Austin, Texas had been paying every bill on time and keeping balances low while saving for a home. One morning her score dropped 28 points with no obvious reason. The stress was intense — she worried higher rates would make her dream home unaffordable and delay her family’s plans by months. Once she understood the Statement Snapshot Effect and Utilization Creep Pattern, she started making mid-cycle payments and monitoring trends. Within 60 days her score recovered, and she moved forward with confidence.

Marcus in Portland, Oregon opened a new credit card for a 0% balance transfer offer and paid it perfectly. Two months later his score dropped 22 points right before he needed to refinance his car. The uncertainty was exhausting. Learning the New Account Aging Drag and Reporting Lag Surprise helped him see the drop as temporary. Four months later his score had stabilized, and he secured better refinancing terms.

At this point, many people realize they don’t actually have visibility into how their credit is changing day to day. This is where real-time monitoring tools Affiliate Disclosure can quietly make a difference.

Common misunderstandings often make the situation feel worse than it is. Many believe a sudden drop means they must have done something wrong, but most drops result from normal monthly reporting timing. Others assume paying everything off guarantees no drops, ignoring statement balances and reporting lags. Some expect the score to improve the moment they fix a balance, when recovery usually takes 30–90 days of consistent positive data. And many think one drop will permanently hurt their ability to get loans, when most temporary drops recover if underlying behavior stays strong.

Replacing these assumptions with accurate pattern understanding prevents panic and supports smarter decisions.

Strategic takeaways flow naturally from this understanding. Monitor your statement closing dates and consider making extra payments before they arrive when a big application is coming up. Keep individual card utilization low while maintaining a healthy overall rate below 30% (ideally under 10% for major loans). Avoid opening multiple new accounts close together, and review your full credit reports at least twice a year to catch reporting lags or errors early.

These actions work because they respect how the system actually processes timing and data — not because they are shortcuts. For a deeper look at how payment behavior shapes recovery speed, see how payment history affects your score.

To minimize the chance of sudden drops before a major application, group rate shopping within the 14–45 day window and prioritize responsible habits. Positive behaviors like on-time payments and low utilization help the score recover faster than simply waiting for time to pass.

FAQ

Why did my credit score drop for no reason? Your credit score can drop suddenly due to monthly reporting cycles, statement closing dates, small utilization shifts, or new account aging effects. These are normal system reactions to timing rather than major mistakes.

How long does a sudden credit score drop usually last? Most temporary drops begin recovering within 30–90 days as new positive data arrives. Full recovery often occurs within 1–3 months if your underlying payment behavior remains strong.

Can a credit score drop without any late payments? Yes. Common causes include statement balance timing, utilization creep, new account effects, or delayed reporting from creditors — even when you pay everything on time.

Is a sudden credit score drop permanent? No. Most sudden drops are temporary. They usually fade as positive monthly data continues to build, especially with consistent on-time payments and controlled utilization.

How can I prevent unexpected credit score drops? Monitor statement closing dates, make strategic mid-cycle payments when needed, avoid opening multiple new accounts close together, and use real-time monitoring tools Affiliate Disclosure to catch changes early.

Does checking my own credit score cause a drop? No. Soft inquiries (when you check your own score) never affect your credit score.

Will my credit score recover on its own after a sudden drop? Yes, in most cases. Consistent positive behavior (on-time payments and low utilization) usually leads to recovery within 30–90 days.

Should I be worried about a 20–40 point drop? Not necessarily if it’s temporary. Focus on the underlying patterns rather than the number itself. Many drops correct naturally with time and good habits.

How do I know if my credit score drop is serious? Look at the context. If it coincides with high utilization, new accounts, or multiple inquiries, it may take longer to recover. Consistent positive behavior usually resolves most temporary drops.

What should I do if my credit score drops right before a big loan application? Pause unnecessary new applications, make strategic payments before statement dates, and consider real-time monitoring tools Affiliate Disclosure to track changes and timing.

Conclusion

Sudden credit score drops are rarely random. They are the visible result of timing-based patterns interacting within the larger credit system. When you understand these patterns and how they work together, you stop reacting with panic and start managing your credit with confidence.

Your credit score doesn’t drop because you did something wrong — it drops because the system reinterprets the latest monthly snapshots through the lens of timing and context.

This deeper view connects directly to how credit utilization affects your score, how new credit affects your score, and why your credit score changes. The clearer the full picture becomes, the more control you gain over outcomes that once felt random.