Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Mix & Account Types Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Revolving and Installment Accounts Are Interpreted in Credit Scoring Models

Many individuals have a mix of credit accounts — credit cards, auto loans, student loans, mortgages — yet still don’t fully understand how that mix is interpreted.

Credit scoring systems do not simply look at how many accounts you have. They evaluate what types of credit behavior are present, how those behaviors differ, and how they interact over time.

This page explains what credit mix means, how different account types are reported, and how they are interpreted within scoring models such as FICO and VantageScore — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system designed to explain how credit data is interpreted across scoring models.

Who This Page Is For

This page is designed for:

Individuals with both credit cards and loans who want to understand how account diversity is viewed

People with only one type of credit (e.g., only credit cards or only loans) noticing score differences

New credit users building a profile and trying to understand how different accounts appear

Anyone seeking a clear, non-promotional explanation of how credit mix works

This is educational content only — no strategies or recommendations are provided.

In This Guide

What credit mix actually represents

Types of credit accounts

Revolving vs installment credit

How account types are reported

How scoring models interpret credit mix

Behavioral diversity vs account quantity

Common observable patterns

How credit mix interacts with other factors

Monitoring credit mix over time

Frequently asked questions

What Is Credit Mix?

Definition

Credit mix refers to the variety of account types present in a credit profile, such as revolving accounts (credit cards), installment loans (auto, personal, student), and mortgages.

Featured Snippet: What is credit mix in credit scoring?

Credit mix refers to the variety of account types in a credit profile, such as revolving credit and installment loans, and is used in scoring models to evaluate diversity of credit behavior.

🧠 Core Insight: Credit Mix Is Behavioral Diversity

Credit mix is not about how many accounts exist — it is about how many different types of credit behavior can be observed.

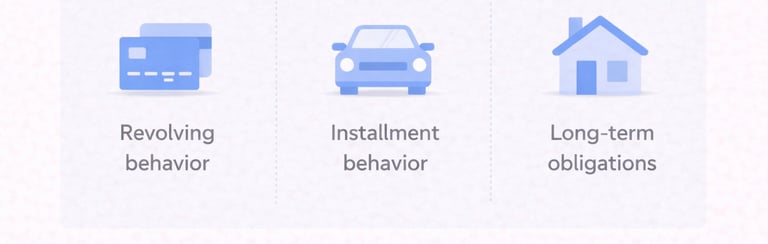

Each account type represents a different pattern:

Revolving accounts → variable balances, flexible repayment

Installment loans → fixed payments over time

Mortgages → long-term structured obligations

Scoring models are not just counting accounts — they are evaluating how many distinct financial behaviors exist within a profile.

This is why two people with the same number of accounts can have very different profiles depending on the types of accounts present.

Types of Credit Accounts

Common account types include:

Revolving credit

(Credit cards, HELOCs)Installment loans

(Auto loans, personal loans, student loans)Mortgage loans

(Primary home loans, home equity loans)Retail/store accounts

(Merchant-specific revolving accounts)Finance company accounts

(Specialized lending institutions)

Each of these contributes a different behavioral pattern to the overall profile.

Revolving vs Installment Credit

Revolving Credit

Borrow up to a limit

Balance can increase or decrease

Minimum payments required

Utilization is calculated (balance ÷ limit)

Installment Credit

Fixed amount borrowed

Fixed monthly payment

Defined payoff timeline

No utilization ratio

🧠 Key Distinction

Revolving credit shows how you manage ongoing access to credit

Installment credit shows how you manage structured repayment over time

These are fundamentally different behaviors — and are evaluated differently.

How Credit Mix Is Reported

Credit account types are reported to credit bureaus by creditors using standardized data fields:

Account type classification

Open date

Balance and limit (for revolving)

Payment status

Account status (open, closed, paid)

Scoring models analyze the presence, distribution, and interaction of these account types — not just their existence.

Credit Mix in Scoring Models

FICO Models

Credit mix accounts for approximately 10% of the score

“Credit mix accounts for about 10% of your score.” — myFICO.com

VantageScore 4.0

Credit mix is included within Depth of Credit (~20%)

Greater emphasis on overall profile structure and diversity over time

Featured Snippet: How important is credit mix?

Credit mix accounts for approximately 10% in FICO models and is included within depth of credit (~20%) in VantageScore models.

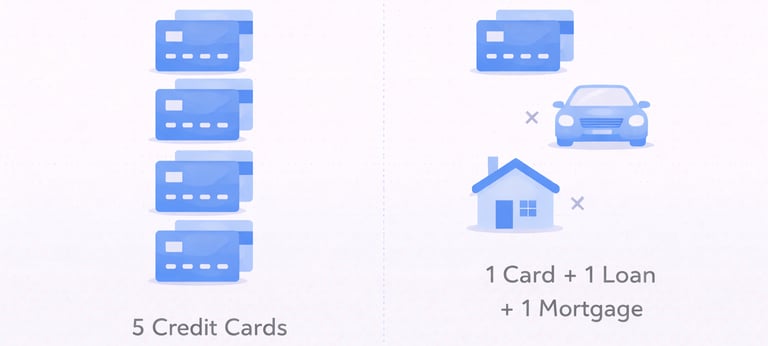

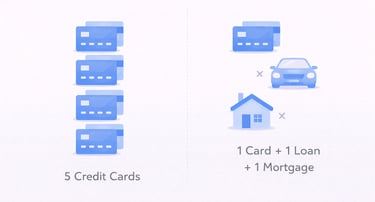

Credit Mix vs Credit Quantity

Credit mix is about variety, not volume.

Multiple credit cards = same behavior type

One credit card + one auto loan = two behavior types

Adding more of the same account type does not significantly increase behavioral diversity.

This is one of the most misunderstood aspects of credit scoring.

Common Observable Patterns in Credit Mix

Based on historical model data, patterns often observed include:

Profiles with both revolving and installment accounts appear more developed

Profiles with only one type may show more variability

Adding a new account type may correspond with temporary changes

Mixed profiles (revolving + installment + mortgage) may appear more stable over time

These are patterns observed in model data — not rules or guarantees.

How Credit Mix Interacts With Other Factors

Credit mix does not function independently. It interacts with:

Credit age

→ New account types may reduce average ageNew credit activity

→ Adding a new type often involves an inquiry

See Credit Inquiries & New Credit Activity FrameworkCredit utilization

→ New revolving accounts affect utilization ratios

See Credit Utilization & Credit Card Behavior guideNegative items

→ Behavior across different account types may be evaluated differently

See Credit Report & Negative Items FrameworkScore fluctuations

→ New account types can influence short-term changes

See Credit Score Changes & Fluctuations Framework

Why Credit Mix Contributes to Profile Structure

Credit mix helps define the structure of a credit profile, not just its performance.

It allows scoring models to evaluate:

Behavioral diversity

Long-term consistency across account types

Ability to manage different forms of credit

This contributes to how complete or “developed” a credit profile appears in model data.

👁️ Viewing Credit Mix in Your Profile

Credit mix is reflected in how different account types are reported within your credit file, including revolving accounts, installment loans, and other account categories.

Because these account types are recorded over time, reviewing your credit profile can help clarify how different types of credit are represented and how they interact within your overall credit data.

For example, your profile may show a combination of credit cards, loans, and other accounts, each contributing a different type of behavior pattern. Observing how these accounts are reported can help connect how credit mix is interpreted within scoring models as part of a broader system.

Credit Monitoring Tool

Review your account types, balances, and overall credit profile structure

👉 View your full credit profile and account mix Affiliate disclosure

This tool allows monitoring of reported account types, but scores and interpretations may vary depending on model, bureau, and timing.

Related Guides

👉 Complete Credit Scoring Education Framework

👉 Credit Age & File Depth Framework

👉 Credit Inquiries & New Credit Activity Framework

👉 Credit Utilization & Credit Card Behavior

👉 Credit Score Changes & Fluctuations Framework

Key Takeaway

Credit mix reflects the variety of credit behaviors present in a profile — not just the number of accounts.

It contributes to how scoring models interpret:

Behavioral diversity

Profile structure

Long-term stability

It is one component of a broader system that evaluates credit data over time.

Frequently Asked Questions (FAQ)

What is credit mix?

Credit mix refers to the variety of account types in a credit profile, such as credit cards, loans, and mortgages.

Does credit mix affect credit scores?

Yes, it is a smaller factor — approximately 10% in FICO and part of depth of credit in VantageScore.

What is the difference between revolving and installment credit?

Revolving credit allows flexible borrowing up to a limit, while installment credit involves fixed payments over a set period.

Does having more accounts improve credit mix?

Not necessarily — variety of account types matters more than quantity.

Does opening a new loan change credit mix?

Adding a new type of account may increase diversity, but may also affect other factors like age and inquiries.

Do closed accounts still count toward credit mix?

Closed accounts may continue to contribute to the overall profile depending on the model and reporting.

Is credit mix more important than payment history?

No, payment history is generally the most significant factor in scoring models.

Can credit mix change over time?

Yes, as new account types are added or older accounts age or close.

← Previous Step: Credit Age & File Depth

Next Step → Credit Inquiries & New Credit Activity

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com does not: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion Or consult a qualified professional.