Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Utilization Explained: How Revolving Credit Usage Is Interpreted in Credit Scoring Models

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

Credit utilization is one of the most commonly discussed — and often misunderstood — parts of credit scoring.

If you’ve ever looked at your credit report and wondered why your score changed even though you paid on time, utilization is often part of that story.

This guide explains what credit utilization is, how it’s calculated, and how it shows up in scoring models like FICO and VantageScore — in a clear, non-promotional way.

Who This Page Is For?

This page is designed for:

People reviewing their credit report and noticing changes in balances or utilization

Individuals with consistent payment history who want to understand how credit card usage is interpreted

New credit users learning how credit cards impact scoring models

Anyone looking for a clear, neutral explanation of how utilization works

This is an educational guide only — no strategies, services, or guarantees are provided.

What You’ll Learn About Credit Utilization

What credit utilization is

How it’s calculated

How scoring models interpret it

The difference between overall and individual utilization

Why utilization can change even when your behavior doesn’t

How it appears on credit reports

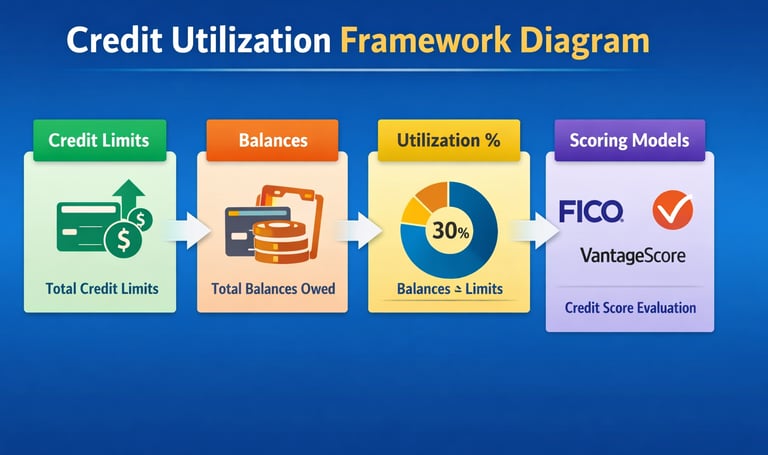

What Is Credit Utilization?

Credit utilization is the percentage of your available credit that you’re currently using.

It only applies to revolving accounts, like credit cards — not installment loans such as mortgages or auto loans.

Simple example:

Credit limit: $1,000

Balance: $300

Utilization: 30%

In short, it’s a way of measuring how much of your available credit is being used at a given time.

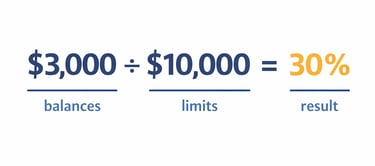

How Credit Utilization Is Calculated

The calculation is straightforward:

Total credit card balances ÷ total credit limits = utilization percentage

Example:

Total balances: $3,000

Total limits: $10,000

Utilization: 30%

But scoring models don’t just look at one number.

They typically evaluate:

Your overall utilization across all accounts

Your utilization on each individual account

How many accounts are carrying balances

How Utilization Is Interpreted in Scoring Models

Credit scoring models use utilization as part of a broader evaluation of credit behavior.

FICO Models

Utilization falls under the “amounts owed” category

This category makes up roughly 30% of the score

VantageScore Models

Utilization is part of a category weighted around 20%

These models may place more emphasis on trends over time

Rather than focusing on a single moment, scoring systems often consider patterns and changes in utilization over time.

Overall vs. Individual Utilization

Utilization is evaluated in more than one way:

1. Overall Utilization

This is your total balances compared to your total limits across all cards.

2. Individual Utilization

This looks at each card separately — how much of that specific limit is being used.

3. Accounts With Balances

Models may also consider how many of your accounts currently have a balance.

Why this matters:

It’s possible to have a low overall utilization but still have one card that is heavily used — and both can be evaluated.

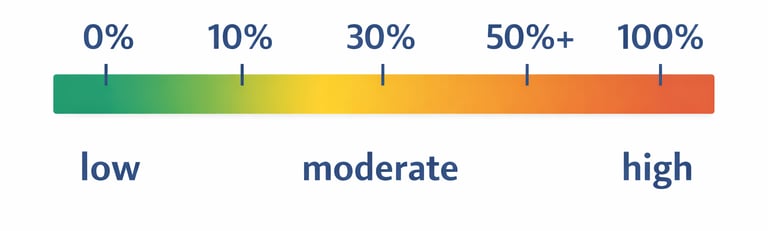

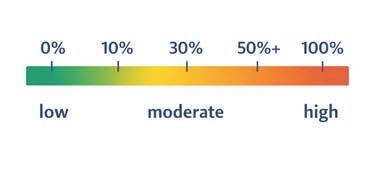

Common Utilization Patterns (Observed in Data)

While there are no official “cutoffs,” patterns are often observed in historical scoring data:

Below ~10% → Often associated with higher scores

10–30% → Common moderate range

Above ~30% → Often associated with lower scores

Above 50–70% → Frequently linked with stronger negative impact

These are general observations — not fixed rules used by scoring models.

Balances vs. Credit Limits (Why the Relationship Matters)

Utilization is driven by the relationship between:

Balances (what you owe)

Credit limits (what you’re allowed to borrow)

Changes in either one can affect your utilization:

Higher balances → higher utilization

Higher limits (with same balance) → lower utilization

This is why utilization can change even if your spending habits stay the same.

Why Utilization Changes (Even Without New Spending)

Many people notice their utilization changes unexpectedly.

This usually comes down to timing and reporting:

Lenders typically report balances once per month

The reported balance may be before or after a payment is made

Statement timing can shift what gets reported

Credit limits can change

Because of this, utilization can fluctuate without any real change in long-term behavior.

How Utilization Works Over Time

Utilization isn’t static — it updates as new data is reported.

Factors that influence it include:

Monthly reporting cycles

Payment timing

Changes in spending

Adjustments to credit limits

Some scoring models also consider recent trends, not just the current snapshot.

Multiple Accounts and Added Complexity

If you have multiple credit cards, utilization becomes more layered.

Scoring models may evaluate:

Total utilization across all accounts

Individual card utilization

How balances are distributed

In some cases:

A few highly utilized accounts may stand out

Different balance distributions may produce different outcomes

Monitoring Credit Utilization

Many people track utilization using tools like:

Credit Karma (VantageScore-based data)

Experian (FICO-based data in some cases)

These tools show how your reported balances and limits change over time.

Differences between platforms can occur due to:

Different data sources

Different scoring models

Different update timing

How Utilization Fits Into the Bigger Picture

Credit utilization is just one part of a larger system.

Scoring models also consider:

Payment history

Credit age

Account mix

Recent activity

To see how everything connects, refer to the full Credit Scoring Education Framework, where utilization is explained alongside all other factors.

Monitoring Utilization Data

Some individuals choose to periodically review their credit reports and scores to observe how balances, limits, and utilization are reported over time.

Because credit utilization is based on reported data — not real-time behavior — what appears in a credit profile reflects how and when information is submitted by lenders. Reviewing this data directly can help connect utilization concepts to actual account activity.

For example, utilization may appear differently depending on when balances are reported within a billing cycle, how multiple accounts are carrying balances, and how total utilization compares to individual account usage. Observing these variations can make it easier to understand how utilization is interpreted across scoring models.

In addition, reviewing your credit profile can provide insight into how changes in balances, payments, or credit limits affect utilization as new data is reported. This helps illustrate how utilization functions as part of a broader pattern over time rather than a fixed number.

Credit Monitoring Tool

Review your balances, limits, and utilization across accounts in one place.

👉 View your full credit profile and utilization Affiliate disclosure

This allows individuals to observe how credit utilization is reported and how it may change over time. It’s important to note that the specific score or utilization displayed can vary depending on the scoring model used, the credit bureau providing the data, and the timing of updates.

👉 Learn how utilization appears in real credit reports in our Credit Monitoring & Credit Tools guide

👉 See how utilization fits into the full system in the Complete Credit Scoring Education Framework

Key Takeaway

Credit utilization reflects how much of your available credit is being used at a specific point in time.

It’s one part of a larger system that evaluates credit behavior across multiple factors — not a standalone measurement.

Frequently Asked Questions (FAQ)

What is credit utilization?

Credit utilization simply means how much of your available credit you’re using. It’s usually shown as a percentage — for example, using $500 out of a $1,000 limit = 50% utilization.

How is credit utilization calculated?

It’s calculated by dividing your total credit card balances by your total credit limits. So if you have $2,000 in balances and $10,000 in limits, your utilization is 20%.

What is considered a “good” credit utilization ratio?

There’s no exact number that works for everyone, but in general:

👉 Lower utilization is often associated with better credit scores

Does credit utilization affect your credit score?

Yes — utilization is one of the key factors used in credit scoring models.

It helps indicate how heavily you rely on your available credit.

What happens if your credit utilization is high?

Higher utilization (using a large portion of your credit) is often linked with lower credit scores in historical data.

It can signal higher risk to lenders.

Does paying off credit cards lower utilization?

Yes — when you pay down your balances, your utilization typically goes down once the new balance is reported.

How often is credit utilization updated?

Most lenders report your balances once a month, so your utilization can change monthly based on what’s reported.

Does closing a credit card affect utilization?

It can. Closing a card reduces your total available credit, which may increase your utilization percentage — even if your spending doesn’t change.

What matters more: individual cards or overall utilization?

Both matter.

Scoring models usually look at:

Your overall utilization across all cards

And how much you’re using on each individual card

Can credit utilization change every month?

Yes — it can change anytime your balances or credit limits change and get reported.

What is revolving credit?

Revolving credit is credit you can reuse, like credit cards.

You can borrow up to a limit, pay it down, and use it again.

Does utilization apply to loans like mortgages or car loans?

No — utilization only applies to revolving accounts like credit cards, not installment loans.

Why does utilization matter so much?

Because it shows how much of your available credit you’re using.

This helps scoring models estimate risk based on borrowing behavior.

Can opening a new credit card lower utilization?

It can.

A new card increases your total credit limit, which may lower your overall utilization — as long as your balances stay the same.

Why does my utilization look different on different apps?

Different apps may:

Update at different times

Use different data sources

Or show estimates instead of real-time data

So it’s normal to see small differences.

← Previous Step: Payment History & Delinquency Patterns

Next Step → Credit Age & File Depth

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Different tools may use different scoring models or data sources, which can result in variations in reported utilization or scores.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT OFFER CREDIT REPAIR SERVICES, DISPUTE CREDIT REPORT ITEMS, OR PROVIDE ANY FORM OF CREDIT IMPROVEMENT ASSISTANCE. ACCURATE NEGATIVE INFORMATION CANNOT BE REMOVED FROM CREDIT REPORTS UNDER FEDERAL LAW. FOR QUESTIONS ABOUT YOUR PERSONAL CREDIT REPORT OR SCORE, CONTACT THE CREDIT BUREAUS (EQUIFAX, EXPERIAN, TRANSUNION) DIRECTLY OR CONSULT A QUALIFIED PROFESSIONAL.