Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Age & File Depth Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Length of Credit History and Account Age Are Interpreted in Credit Scoring Models

Many individuals maintain consistent payment history and reasonable balances, yet still observe lower-than-expected scores or more volatility than anticipated.

A common reason for this is credit age and file depth — not just what has happened in a credit profile, but how long it has been observed and how much data exists.

Credit scoring systems evaluate patterns over time, not just individual events.

This page explains how credit age and file depth are calculated, how they are interpreted within scoring models such as FICO and VantageScore, and how they interact with other credit data — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system explaining how credit data is interpreted across scoring models.

🧠 Who This Page Is For

This page is designed for:

- Individuals new to credit (young adults, immigrants, or first-time users)

- People with thin credit files who notice more volatility

- Individuals opening new accounts and observing unexpected score changes

- Anyone seeking a clear, factual understanding of how credit age is interpreted

This page provides educational context only, not recommendations or strategies.

📊 In This Guide

- What credit age and file depth represent

- How credit age is calculated

- Core components of credit age

- How scoring models interpret time-based data

- Thin vs thick credit files

- How credit age evolves over time

- Common observable patterns

- How credit age interacts with other factors

- Why credit age contributes to stability

- Monitoring credit age

- Frequently asked questions

📌 What Is Credit Age and File Depth?

Definition

Credit age refers to how long credit accounts have been established and active.

File depth refers to the amount of credit data available over time, including the number of accounts and their duration.

These factors do not measure behavior directly.

They measure how long behavior has been observed and how much data exists to evaluate it.

A profile with identical behavior but different history length will often be interpreted differently because the data depth is different.

Featured Snippet:

Credit age refers to how long credit accounts have been established and active, and is used by scoring models to evaluate long-term credit behavior patterns.

🧠 Core Insight: What Credit Age Actually Measures

Credit age does not measure how well someone manages credit.

It measures how long that behavior has been observed and recorded.

Two individuals may behave the same today, but if one has 2 years of history and another has 15 years, scoring models interpret those profiles differently because the time-based data is not equal.

Credit age functions as a time-based validation layer, not a behavior score.

🔢 How Credit Age Is Calculated

Credit age is derived from multiple time-based metrics:

- Age of oldest account

- Age of newest account

- Average age of accounts

- Overall file depth

These values are based on account open dates reported by creditors and updated over time.

🧩 Core Components of Credit Age

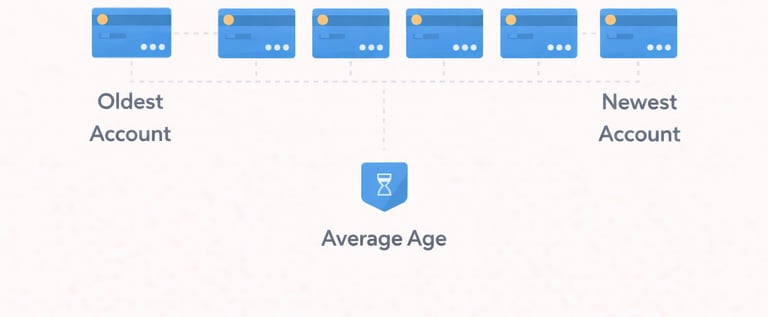

1. Oldest Account Age

The earliest account on file, which anchors the timeline of the credit profile.

2. Average Age of Accounts

The average age across all accounts, which adjusts when new accounts are added.

3. Account Age Distribution

The mix of older and newer accounts within the profile.

4. File Depth

The number of accounts and the overall thickness of credit history over time.

Closed accounts may continue contributing to age calculations in many scoring models.

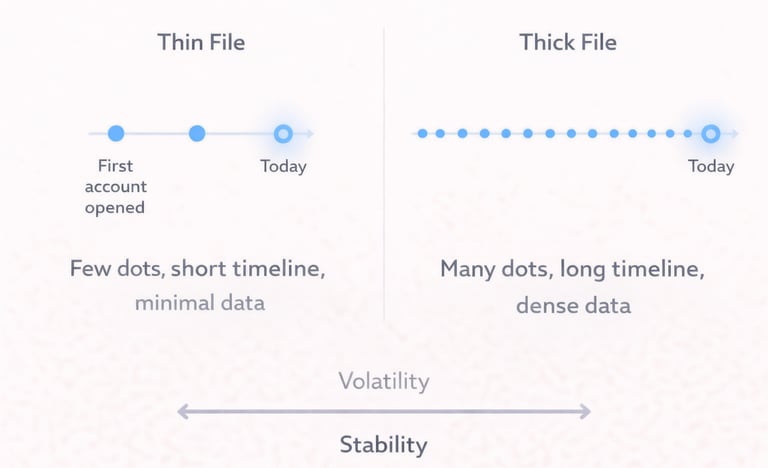

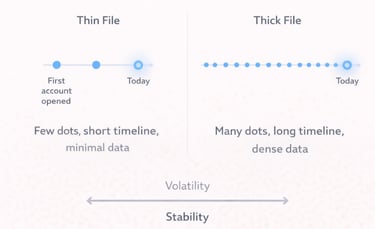

📊 Thin vs Thick Credit Files (Data Depth Dynamics)

Credit profiles are often described as “thin” or “thick,” referring to how much data exists.

A thin file typically has:

- Few accounts

- Short history

- Limited data points

A thick file typically has:

- Multiple accounts over time

- Longer history

- More data available for evaluation

This difference affects how scores behave:

- Thin files may show greater volatility because each change represents a larger portion of total data

- Thick files tend to show more stability because changes are absorbed within a larger dataset

This explains why similar behavior can produce different score movements across profiles.

🧠 Credit Age in Scoring Models

FICO Models

Credit age accounts for approximately 15% of the score.

VantageScore 4.0

Depth of credit (age + file depth) accounts for approximately 20%.

These models use time to evaluate stability, consistency, and long-term patterns.

Featured Snippet:

Credit age and file depth account for approximately 15% in FICO models and around 20% in VantageScore 4.0.

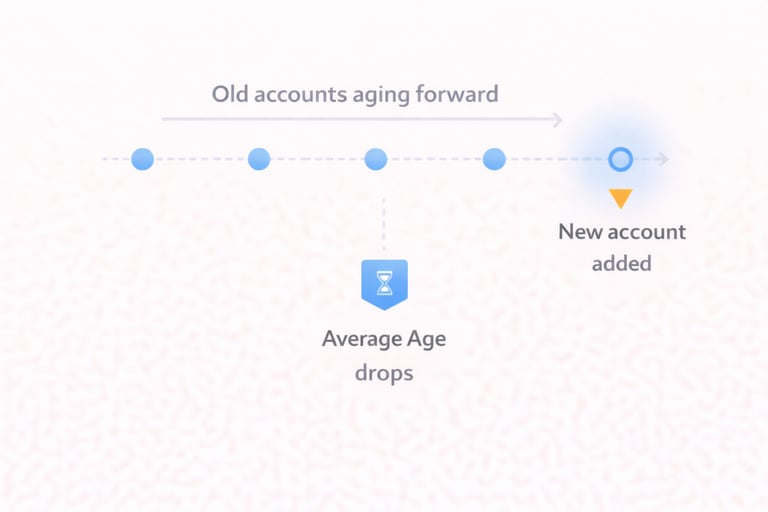

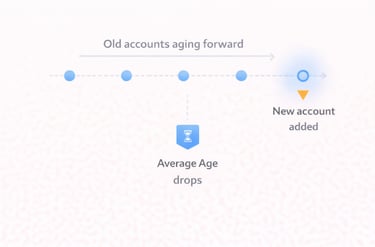

🔄 How Credit Age Changes Over Time

Credit age evolves continuously:

- Opening a new account lowers average age

- Time increases the age of all accounts

- Closed accounts often still contribute

- Older accounts help stabilize the profile

Key Concept:

Credit scores are recalculated from updated data — not gradually adjusted.

Featured Snippet:

Opening a new account lowers average age when reported and may be associated with temporary changes in scoring models.

⚙️ Credit Age as a Stability Signal

Credit age functions as a stability signal within scoring models.

It provides context for:

- Consistency over time

- Reliability of repayment patterns

- Stability across different periods

Longer timelines allow scoring models to evaluate behavior across more conditions, which contributes to more stable interpretations.

📊 Common Observable Patterns

Frequently observed patterns include:

- Longer credit history often aligns with more stable scores

- Thin credit files may show more volatility

- Multiple new accounts may correspond to temporary changes

- Mixed age profiles may be interpreted differently

These patterns reflect how models interpret time-based data.

🔗 How Credit Age Interacts With Other Factors

Credit age interacts with multiple parts of the system:

- New credit activity → lowers average age

- Negative items → impact may change as they age

- Credit utilization → may shift alongside new accounts

- Score changes → often involve multiple variables

👉 See related pages:

- Credit Inquiries & New Credit Activity Framework

- Credit Report & Negative Items Framework

- Credit Utilization & Credit Card Behavior

- Credit Score Changes & Fluctuations Framework

Important: Most score changes are the result of multiple factors interacting at the same time.

🧠 Why Credit Age Contributes to Stability

Credit scoring models rely on pattern recognition over time.

Time allows models to evaluate:

- Consistency

- Stability

- Long-term behavior patterns

More history = more data

More data = more confidence in the evaluation

👁️ Viewing Credit Age in Your Profile

Credit age is based on the length of time accounts have been reported, which means it reflects historical data rather than recent activity alone.

Because this information builds over time, reviewing your credit profile can provide a clearer picture of how account age, average age of accounts, and account timelines are represented across your credit file.

For example, the age of your oldest account, the average age of all accounts, and the timing of newly opened accounts may all appear differently depending on how your credit history has developed over time.

Observing these details directly can help connect how credit age is interpreted within scoring models as part of a broader long-term pattern.

Credit Monitoring Tool

Review your account history, timelines, and age of accounts across your credit profile

👉 View your full credit profile and account history Affiliate disclosure

🔑 Key Takeaway

Credit age and file depth reflect how long credit behavior has been observed.

They help scoring models evaluate stability, consistency, and long-term patterns within a broader system of credit data interpretation.

❓ Frequently Asked Questions (FAQ)

What is credit age?

Credit age refers to how long credit accounts have been established.

What is average age of accounts?

The average age across all accounts on a credit report.

Does opening a new account lower credit age?

Yes, it lowers the average age when reported.

Do closed accounts still count?

Closed accounts often continue contributing in many models.

How important is credit age?

Approximately 15% in FICO and about 20% in VantageScore 4.0.

What is a thin credit file?

A credit profile with limited accounts or short history.

Does credit age affect score changes?

Changes in age may be associated with score fluctuations.

Can older accounts stabilize a profile?

Longer history is often associated with more stable patterns.

← Previous Step: Credit Utilization & Card Behavior

Next Step → Credit Mix & Account Types

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion, Or consult a qualified professional.