Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Monitoring & Credit Tools Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Individuals Observe Reported Credit Data Over Time

Credit monitoring tools are a window into the credit scoring system — they provide visibility into reported data such as balances, limits, inquiries, negative items, and calculated scores, allowing individuals to observe how credit information appears and changes over time.

Rather than influencing credit scores directly, these tools reflect how data is reported, updated, and interpreted within scoring models.

This page explains how monitoring tools work, what they typically display, why scores and data can differ across tools, and how monitoring fits into the broader credit data system — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system explaining how credit data is interpreted across scoring models.

Who This Page Is For?

This page is designed for:

Individuals who want to observe their reported credit data over time

People reviewing credit reports and scores from different sources

Those exploring tools that provide visibility into credit information

Anyone seeking factual information about credit monitoring and related tools

This page provides educational context only, not recommendations or strategies.

In This Guide

What is credit monitoring?

How credit monitoring tools work

Common types of monitoring tools

What monitoring tools typically show

Why scores and data differ across tools

How monitoring relates to scoring models

Data lag vs real-time perception

Common observable patterns in monitored data

Frequently asked questions

What Is Credit Monitoring?

Definition

Credit monitoring is the process of regularly reviewing credit reports and scores to observe reported information, such as balances, limits, inquiries, negative items, and calculated scores.

Monitoring tools provide access to certain credit data from one or more bureaus and often include alerts when changes are detected.

Featured Snippet:

Credit monitoring is the process of regularly reviewing credit reports and scores to observe reported information, such as balances, limits, inquiries, negative items, and calculated scores.

How Credit Monitoring Tools Work

Credit monitoring tools connect to credit bureau data (Equifax, Experian, TransUnion) and provide access to:

Reported credit information

Calculated scores (VantageScore, FICO, or model-based estimates)

Alerts for changes in reports or scores

Tools vary in:

Which bureaus they access

Which scoring models they use

Frequency of updates

Additional features (such as identity monitoring or alerts)

It’s important to understand that these tools display data — they do not control or modify it.

Common Types of Monitoring Tools

Free monitoring services (e.g., Credit Karma, Credit Sesame, WalletHub):

Provide access to scores and reports from one or more bureaus, often using VantageScore models.Paid monitoring services (e.g., myFICO, Experian IdentityWorks):

Provide official FICO scores, three-bureau reports, and additional features such as identity monitoring.

Each type serves a different purpose within the broader ecosystem of credit visibility.

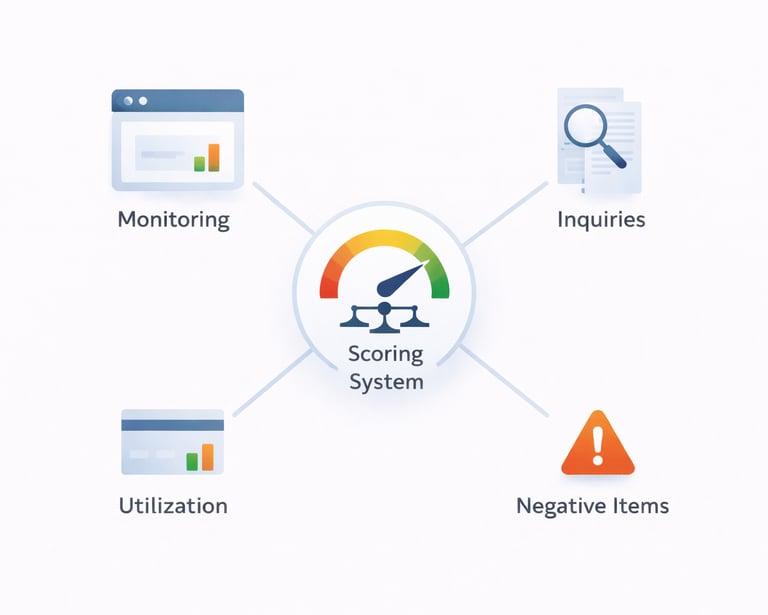

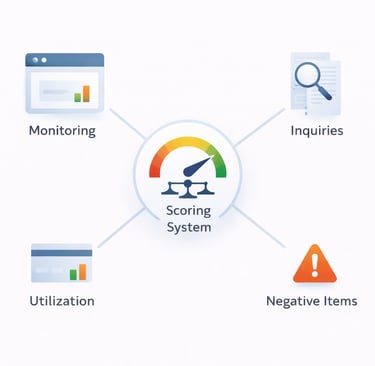

What Monitoring Tools Typically Show

Most monitoring tools display:

Reported balances and credit limits (utilization)

Payment history and negative items

Inquiries (hard and soft)

Calculated scores (VantageScore, FICO, or estimates)

Alerts for changes in reports or scores

These elements reflect what has been reported to credit bureaus — not necessarily real-time financial activity.

Why Scores and Data Differ Across Tools

One of the most common points of confusion is seeing different scores across different platforms.

This happens because:

Different tools use different scoring models (FICO vs VantageScore vs proprietary models)

Different bureaus provide different data snapshots

Updates occur at different times across platforms

Some tools display estimates rather than lender-used scores

These differences are not errors — they reflect how credit data is modeled, sourced, and timed.

How Monitoring Relates to Scoring Models

Monitoring tools display outputs generated by scoring models, but they do not influence those models.

The score you see depends on:

The scoring model used (FICO vs VantageScore)

The bureau providing the data

The timing of the data snapshot

Monitoring provides visibility into how your credit data is being interpreted — but it is not part of the scoring process itself.

Data Lag vs Real-Time Perception

A key concept in understanding monitoring tools is data lag.

Credit data is not real-time:

Lenders typically report data on monthly cycles

Credit bureaus update reports after receiving that data

Monitoring tools display the most recent available snapshot

This means:

A recent payment may not appear immediately

A balance reduction may not reflect until the next reporting cycle

Different tools may show slightly different versions of the same data

This delay often creates the perception that scores are changing unpredictably, when in reality they are reflecting timing differences in reported data.

Common Observable Patterns in Monitored Data

Individuals who monitor their credit over time often observe patterns such as:

Utilization changes based on reported balances and limits

New inquiries appearing after credit applications

Negative items remaining visible for defined reporting periods

Score fluctuations tied to reporting cycles and timing

These patterns reflect how credit data moves through the reporting system and is interpreted by scoring models.

🔍 Choosing the Right Way to Monitor Your Credit

Credit monitoring tools serve different purposes depending on what you are trying to observe.

Some individuals simply want to view their reported credit data. Others want to track changes over time, while some are exploring what financial options may be available based on their current profile.

Understanding these differences can help clarify which type of tool aligns with what you’re looking to observe.

🟢 Viewing Your Credit Profile

For individuals who want to see their reported credit data — including balances, limits, inquiries, and negative items — a monitoring tool can provide a direct view into how this information appears across your credit file.

Credit Monitoring Tool

Review your full credit profile, including reported balances, account activity, and credit data

👉 View your full credit profile and reported data Affiliate disclosure

🟣 Tracking Changes Over Time

Because credit data updates in cycles, some individuals choose to track how their credit profile changes over time, including score fluctuations, reporting updates, and account activity.

Observing these patterns can help illustrate how scoring models respond to different types of data updates rather than focusing on a single moment.

Advanced Credit Tracking Tool

Track score changes, reporting updates, and account activity over time

👉 Track your credit changes and score behavior over time Affiliate Disclosure

These tools allow observation of reported data, but exact scores and data may vary depending on the model, bureau, and timing of updates.

How This Fits Into the Full Credit System

Monitoring tools are not a separate system — they are a view into the broader credit system.

They reflect how data from:

Credit utilization

Payment history

Credit age

New credit activity

- is reported and interpreted.

👉 See the full system in the Complete Credit Scoring Education Framework

👉 See how utilization appears in monitored data in Credit Utilization & Credit Card Behavior

👉 See how negative items are tracked in Credit Report & Negative Items Framework

👉 See how inquiries appear in Credit Inquiries & New Credit Activity Framework

Key Takeaway

Credit monitoring tools provide visibility into reported credit data over time. They allow individuals to observe how balances, limits, inquiries, and negative items appear within credit reports, but the scores and data displayed may vary depending on the scoring model, bureau, and timing of updates.

Frequently Asked Questions (FAQ)

What is credit monitoring?

Credit monitoring is the process of regularly reviewing credit reports and scores to observe reported information over time.

How do credit monitoring tools work?

They connect to credit bureau data and display reported information, calculated scores, and alerts for changes.

What do monitoring tools typically show?

Balances, limits, inquiries, negative items, and calculated scores.

Are free monitoring tools accurate?

They display real reported data, but scores may vary depending on the model used.

Do monitoring tools affect credit scores?

No — they only display data and calculated scores.

Why do scores differ between tools?

Different models, bureaus, and update timing create variations.

How often do monitoring tools update?

Typically daily to weekly depending on the tool and bureau.

Can monitoring tools show all three bureaus?

Some do, while others show one or two.

Are monitoring tools the same as credit repair services?

No — monitoring tools display data, while credit repair services attempt to change reported data.

← Previous Step: Credit Score Changes & Fluctuations

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT OFFER CREDIT REPAIR SERVICES, DISPUTE CREDIT REPORT ITEMS, OR PROVIDE ANY FORM OF CREDIT IMPROVEMENT ASSISTANCE. ACCURATE NEGATIVE INFORMATION CANNOT BE REMOVED FROM CREDIT REPORTS UNDER FEDERAL LAW. FOR QUESTIONS ABOUT YOUR PERSONAL CREDIT REPORT OR SCORE, CONTACT THE CREDIT BUREAUS (EQUIFAX, EXPERIAN, TRANSUNION) DIRECTLY OR CONSULT A QUALIFIED PROFESSIONAL.