Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer.

The Complete Credit Scoring Education Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

FICO, VantageScore, Credit Reports & Data Explained

Many individuals review their credit report and see numbers they do not fully understand. Even with consistent payment history, scores may appear lower or different than expected. According to Federal Reserve reporting, a substantial share of U.S. adults have limited emergency savings, highlighting how credit access and credit scores can affect everyday financial stability.

This guide explains how credit scoring models interpret data, what factors are included, and how credit reports are used to generate scores — without offering advice, services, or guarantees.

Credit scores are not judgments.

They are mathematical outputs based on historical data patterns.

In This Guide

What is a credit score?

How credit scoring models work

FICO vs. VantageScore

What is inside a credit report

Key factors that influence scores

Credit score ranges explained

Credit utilization explained

How scores change over time

Common observable credit patterns

Common credit scenarios

Why scores vary

Monitoring tools and data access

Frequently asked questions

Who This Framework Is For?

This educational framework is designed for individuals who want to better understand how credit scoring systems interpret data — without sales pressure, services, or personalized recommendations.

It may be especially relevant for:

Individuals reviewing their credit report and feeling confused by the numbers or structure

People with generally consistent payment history who notice scores that seem lower than expected

New credit users trying to understand how credit systems work for the first time

Adults managing credit cards, loans, or multiple accounts who want neutral, factual context

Individuals interested in how lenders interpret credit data through scoring models

Anyone seeking clear, non-promotional education about credit reports, scoring factors, and financial data patterns

This framework is not designed to provide strategies, recommendations, or credit improvement guidance, but rather to explain how credit data is structured and interpreted within commonly used scoring models.

What Is a Credit Score?

A credit score is a three-digit number, typically ranging from 300 to 850, generated by credit scoring models to represent perceived credit risk based on information in credit reports.

Featured Snippet: What is a credit score?

A credit score is a three-digit number, usually between 300 and 850, generated by credit scoring models to reflect perceived credit risk based on information in credit reports.

How Credit Scoring Models Work

Credit scoring models are statistical algorithms that analyze information from credit reports. The two primary scoring systems used in the United States are FICO Score and VantageScore. FICO was developed by Fair Isaac Corporation. VantageScore was developed by Equifax, Experian, and TransUnion.

These models:

Analyze historical credit data

Identify statistical patterns

Compare current data to past outcomes

Generate a score based on similarity to those patterns

They do not predict future behavior with certainty.

FICO vs. VantageScore (Side-by-Side Comparison)

FactorFICO (Typical)VantageScore 4.0NotesPayment History~35%~41%Most important factor in bothCredit Utilization~30%~20%Balances relative to limitsCredit Age / Depth~15%~20%Age of accounts and depth of fileNew Credit~10%~11%Recent applications and inquiriesCredit Mix~10%Included in depthVariety of account types

Key Difference:

VantageScore places more emphasis on trends and recent behavior, while FICO is commonly

explained through fixed category weightings.

Featured Snippet: How does VantageScore differ from FICO?

VantageScore places more emphasis on recent behavior and trends over time, while FICO is generally

described using fixed category weightings such as payment history, utilization, and credit age.

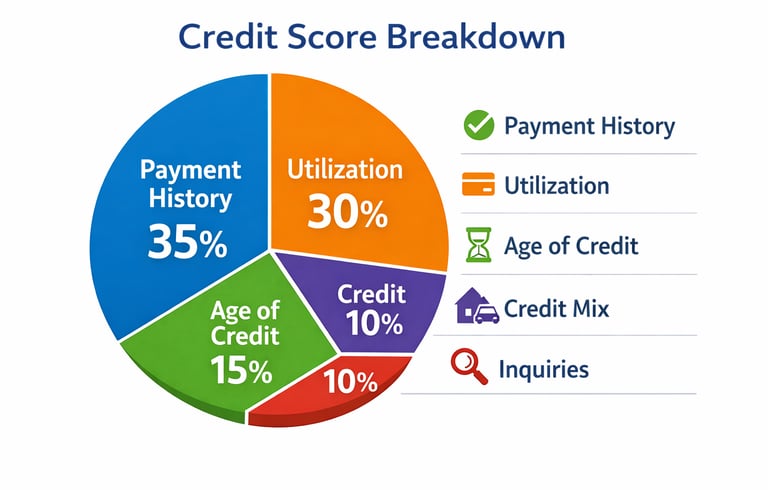

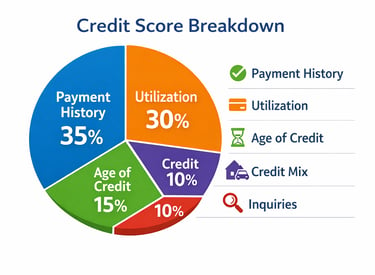

FICO Score – Detailed Breakdown

FICO is the most widely used model in lending decisions. FICO’s published breakdown describes the following approximate categories: payment history 35%, amounts owed 30%, length of credit history 15%, new credit 10%, and credit mix 10%.

VantageScore – Detailed Breakdown

VantageScore 4.0 uses a similar but distinct weighting model:

Payment History – 41%

Depth of Credit – 20%

Credit Utilization – 20%

Recent Credit – 11%

Balances – 6%

Available Credit – 2%

According to VantageScore’s published explanation, the model places greater emphasis on trends over time rather than isolated events.

What Is Inside a Credit Report

Credit reports are compiled by Equifax, Experian, and TransUnion. They commonly include:

Personal identifying information

Account history

Balances and limits

Payment status

Hard and soft inquiries

Certain negative items and public-record-related information, depending on reporting practices and the bureau involved.

Important note on tax liens:

Tax liens may still exist as public records, but they generally do not appear on standard consumer credit reports from the major bureaus today.

Featured Snippet: How can someone get a free credit report?

Individuals can obtain free weekly online credit reports from AnnualCreditReport.com.

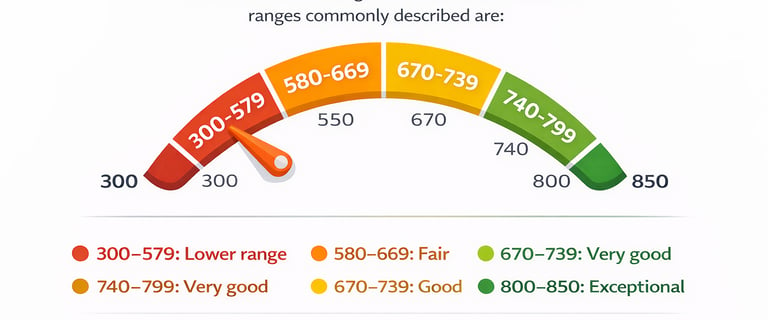

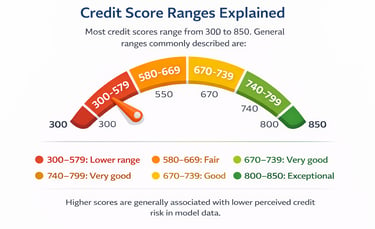

Credit Score Ranges Explained

Most credit scores range from 300 to 850. General ranges commonly described are:

300–579: Lower range

580–669: Fair

670–739: Good

740–799: Very good

800–850: Exceptional

Higher scores are generally associated with lower perceived credit risk in model data.

Credit Utilization – In-Depth Explanation

Credit utilization is the percentage of available revolving credit currently being used. It is generally calculated as total balances divided by total credit limits. High utilization is often associated with lower scores, while lower utilization is often associated with higher scores in model data.

Featured Snippet: What is credit utilization?

Credit utilization is the percentage of available revolving credit currently being used, calculated as total balances divided by total credit limits.

How Credit Scores Change Over Time

Credit scores are dynamic and may change when new information is reported. Factors that may affect scores include:

New account activity

Balance updates

Payment history updates

Aging of negative items

Changes in utilization

Common Observable Credit Report Patterns

Frequently observed patterns include:

Long-term on-time payment history often associated with higher scores

High utilization often associated with lower scores

Multiple recent hard inquiries often associated with temporary score changes

Collections, charge-offs, and bankruptcies often associated with lower scores for extended periods.

Featured Snippet: How long do negative items stay on a credit report?

A credit reporting company generally can report most negative information for seven years. Bankruptcies can remain for up to ten years.

Common Credit Scenarios

Examples often observed in credit data include:

Consistent payments but lower-than-expected scores

High balances despite stable income

Limited credit history in new users

Score changes after accounts are paid off

These scenarios reflect how scoring models interpret data patterns rather than personal intent.

Why Credit Scores Can Vary

Scores may vary depending on:

The model used

The version of the model

The bureau supplying the data

The timing of updates

There is no single universal credit score.

Statistics on Credit Challenges in the U.S.

A substantial share of adults report limited emergency savings.

Many households carry revolving balances and credit card debt.

“Credit scores have become a key gatekeeper to economic opportunity in the United States” is a strong contextual quote, but I would only keep it if you can cite the original interview, paper, or book directly.

Monitoring Services and Accessing Credit Information

Some individuals choose to review their credit information using monitoring services that provide access to reported credit data over time. These services typically display elements such as account balances, credit limits, payment history, inquiries, and calculated scores based on specific scoring models.

Monitoring services do not influence credit scores or change reported data. Instead, they reflect how information has been submitted to credit bureaus and how that data is interpreted within scoring models at a given point in time.

Because credit data is reported in cycles rather than in real time, the information displayed through monitoring services may differ slightly depending on:

The credit bureau providing the data

The scoring model used (FICO, VantageScore, or other variations)

The timing of updates from lenders and data providers

For example, a balance reduction or payment may not appear immediately, and different services may show different score versions based on how data is processed and presented.

Monitoring services are best understood as a window into the credit system, allowing individuals to observe how their credit information appears and changes over time rather than a tool that directly impacts outcomes.

Reviewing credit data periodically can help connect how factors such as utilization, payment history, account age, and inquiries are reflected within a credit profile as new information is reported.

👉 For a deeper explanation of how monitoring tools work and what they display. Continue to the Credit Monitoring & Credit Tools Framework to see how these services display and track real credit data over time.

Monitoring services provide visibility into how credit data is presented, but understanding how that data is interpreted requires examining the broader scoring framework in which it operates.

Frequently Asked Questions

What is a credit score?

A three-digit number representing perceived credit risk based on information in a credit report.

What are the main scoring models?

FICO Score and VantageScore.

How important is payment history?

It is the most significant factor in commonly published FICO and VantageScore explanations.

What is credit utilization?

The ratio of balances to limits on revolving accounts.

Do inquiries affect scores?

Hard inquiries may be associated with temporary score changes.

Are all credit scores the same?

No. Scores vary by model, version, and bureau.

How often do scores update?

Whenever new information is reported or existing information changes.

What is a hard inquiry?

A credit check associated with a credit application.

What is a soft inquiry?

A credit check not associated with a credit application.

Does closing a credit card affect scores?

It may affect utilization and the age profile of available accounts.

Does paying off debt affect scores?

It may reduce utilization, which is often associated with higher scores in model data.

Do tax liens appear on credit reports?

Generally, no on standard consumer reports from the major bureaus today, though tax liens may still exist as public records.

Next Step → Credit Scoring Models

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion Or consult a qualified professional.