Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Data Reporting & Structure Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Credit Data Is Collected, Structured, and Interpreted Within Credit Scoring Systems

Most discussions about credit focus on scores or individual factors.

But before any score exists, there is something more fundamental:

👉 The data itself

Credit scoring models do not create information — they interpret what is reported.

This page explains how credit data is collected, structured, and flows through the system before it is ever evaluated — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system explaining how credit data is interpreted across scoring models.

🧠 Core Insight: The Score Only Knows What Is Reported

Credit scoring models do not see behavior directly — they only see reported data.

Every score is based on:

What is reported

When it is reported

How it is structured

If something is not reported, it does not exist within the scoring system.

Who This Page Is For

This page is designed for:

Individuals trying to understand where credit data comes from

People confused by differences between credit reports or apps

Anyone who wants to understand how the system works behind the scenes

Those looking for a clear, non-promotional explanation of credit data

This is educational content only — no strategies or recommendations are provided.

What Is Credit Data?

Credit data is the structured information reported by creditors about accounts and activity.

This includes:

Account details

Payment status

Balances and limits

Inquiries

Negative items

This data forms the foundation of the entire credit scoring system.

What does “credit data” actually mean in simple terms?

Credit data is simply a record of what has been reported about your accounts.

It’s not your intentions, your income, or your effort — it’s the structured information that lenders send to credit bureaus.

That’s what the system sees and evaluates.

Who Reports Credit Data?

Credit data is reported by:

Credit card issuers

Banks and lenders

Auto and mortgage lenders

Collection agencies

Finance companies

These entities send updates to credit bureaus on a recurring schedule.

Do all lenders report the same way?

No — and this is where a lot of confusion comes from.

Some lenders report to all three bureaus.

Others report to only one or two.

And even when they report to all three, they may do so at different times.

That’s why your reports can look slightly different depending on where you check.

The Role of Credit Bureaus

The three major credit bureaus are:

Equifax

Experian

TransUnion

Their role is to:

Collect reported data

Store and organize it

Provide it to scoring models and platforms

What do credit bureaus actually do?

Credit bureaus don’t decide your score and they don’t judge your behavior.

They act more like large data systems:

collecting information

organizing it

making it available for scoring models to interpret

They are the storage and distribution layer, not the decision-maker.

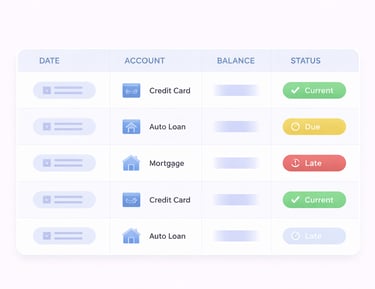

How Credit Data Is Structured

Credit data is not random — it follows a consistent format.

Each account typically includes:

Account type

Open date

Balance

Credit limit (if applicable)

Payment status

Account status

Why does structure matter so much?

Because scoring models don’t read stories — they analyze structured data.

They look at:

patterns

relationships

changes over time

Without consistent structure, the system wouldn’t be able to evaluate anything reliably.

Data Reporting Cycles and Timing

Credit data is not updated in real time.

Typical patterns include:

Monthly reporting cycles

30–45 day update windows

Different timing across lenders

Why doesn’t my credit update immediately?

Because the system runs on reporting cycles.

A payment you make today may not show up until the next reporting cycle.

A balance might be captured before or after a payment depending on timing.

So what you see is always a snapshot, not a live feed.

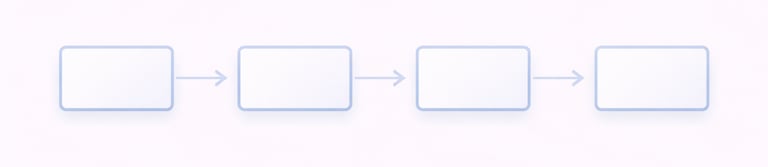

How Data Flows Through the System

The system follows a consistent path:

Creditor → Credit Bureau → Data Storage → Scoring Model → Score Output

How does this actually affect what I see?

It means your score is always based on:

a specific version of your data

at a specific moment in time

Even small timing differences can lead to different results.

🧠 Key Insight: Timing Shapes Perception

Two identical actions can appear differently depending on when they are reported.

Examples:

A payment may be recorded before or after a balance update

A new account may appear on one bureau before another

A balance may look higher or lower depending on the snapshot

This is one of the main reasons credit can feel inconsistent.

Why Data Differences Occur

Differences in reports or scores can result from:

Different reporting schedules

Not all lenders reporting to all bureaus

Timing of updates

Different scoring models

Why do my scores look different on different apps?

Because each app may be using:

a different bureau

a different scoring model

a different update time

So even though the system is consistent, what you see can vary depending on the snapshot being used.

Common Observable Patterns in Credit Data

Over time, many individuals notice patterns such as:

Monthly balance updates

Inquiries appearing shortly after applications

Negative items remaining for set periods

Differences between bureau reports

Are these differences normal?

Yes — these are normal system behaviors.

They don’t mean something is wrong.

They reflect how data is reported, stored, and updated across different systems.

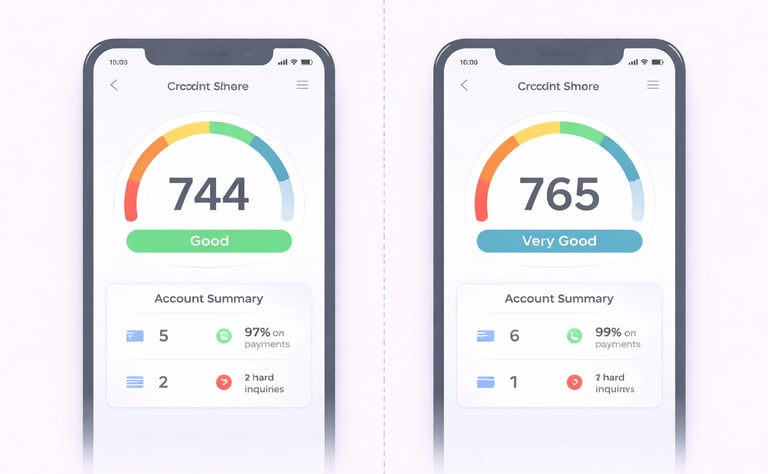

🧠 Observing Credit Data Changes Over Time

Because credit data is reported in cycles rather than in real time, many individuals choose to observe how their credit profile changes over time as new information is submitted, processed, and reflected across different systems.

This is especially relevant when trying to understand how balances, payment updates, inquiries, and account changes appear within a credit file as reporting cycles progress.

For example, a balance update may appear before a payment is reflected, or a new account may show on one bureau before another. These timing differences can create variations in how credit data is displayed at any given moment.

Monitoring services that focus on tracking changes over time can provide a clearer view into how data evolves within the system rather than relying on a single snapshot.

One example of this type of platform is Smart Credit, which emphasizes tracking credit data updates, score changes, and reporting activity as they occur across reporting cycles.

Services like this are designed to help individuals observe:

How credit data updates over time

How score changes correspond to reporting activity

How different updates interact within the same reporting cycle

These platforms do not control or modify reported data. Instead, they provide visibility into how credit information changes and how those changes are reflected within scoring models.

Understanding how data evolves over time can help explain why credit scores may appear to fluctuate and why different snapshots of the same profile can produce different results.

👉 For a deeper look at how tracking tools display changes and patterns over time, continue to the Credit Monitoring & Credit Tools Framework.

Understanding how credit data changes over time provides context for how scoring models respond to updates, rather than focusing on isolated score movements.

Do these tools all show the same information?

Not always.

Each tool may:

use different data sources

update at different times

use different scoring models

They are useful for observation — but not always identical.

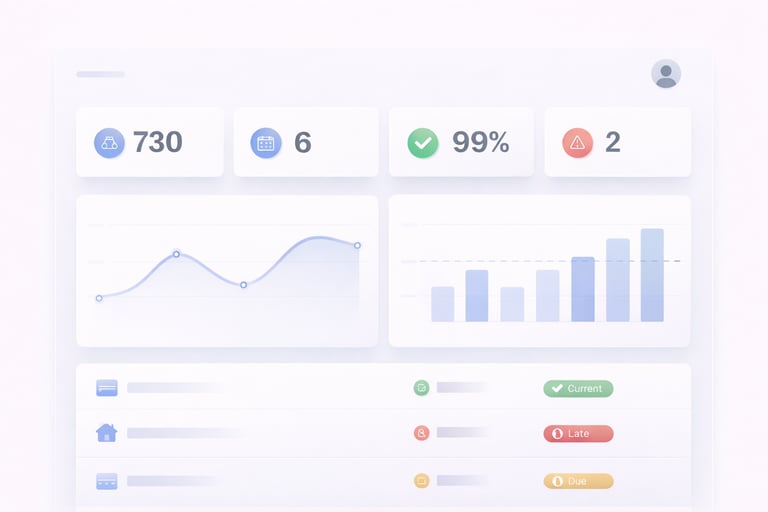

How This Connects to the Full System

Every pillar in the system depends on reported data:

Payment History → based on reported payments

Utilization → based on reported balances

Age → based on reported account dates

Mix → based on account types

Inquiries → based on reported checks

Everything begins with data.

Key Takeaway

Credit scores are built on reported, structured data — not assumptions or real-time behavior.

Understanding the system means understanding:

What is reported

How it is structured

When it is updated

How it flows into scoring models

Frequently Asked Questions

Where does credit data actually come from?

Credit data comes directly from creditors — such as banks, credit card companies, and lenders — who report account activity to credit bureaus on a recurring basis.

Why do different credit reports show different information?

Because not all lenders report to all bureaus, and even when they do, they may report at different times. Each bureau may have a slightly different snapshot of your data.

How often is credit data updated?

Most lenders report monthly, but the exact timing varies. Because of this, updates are not real-time and may take several weeks to appear.

Why do credit scores look different on different platforms?

Different platforms may use different scoring models, bureaus, and update times, which can result in variations in the score displayed.

Do all lenders report to all three credit bureaus?

No — some lenders report to one or two bureaus instead of all three, which can lead to differences between reports.

Why can the same action look different depending on timing?

Because credit data is reported in cycles. A balance or payment may be captured at different points in time, leading to different snapshots.

Can credit data appear in one place but not another?

Yes — due to differences in reporting coverage and timing, data may appear on one bureau but not yet on another.

How does this connect to credit scores?

Credit scores are calculated based on the most recent data available from a specific bureau at a specific time, which is why scores can vary.

← Previous Step: Credit Scoring Models

Next Step → Payment History & Delinquency Patterns

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT OFFER CREDIT REPAIR SERVICES, DISPUTE CREDIT REPORT ITEMS, OR PROVIDE ANY FORM OF CREDIT IMPROVEMENT ASSISTANCE. ACCURATE NEGATIVE INFORMATION CANNOT BE REMOVED FROM CREDIT REPORTS UNDER FEDERAL LAW. FOR QUESTIONS ABOUT YOUR PERSONAL CREDIT REPORT OR SCORE, CONTACT THE CREDIT BUREAUS (EQUIFAX, EXPERIAN, TRANSUNION) DIRECTLY OR CONSULT A QUALIFIED PROFESSIONAL.