Follow the Credit System Step-by-Step

⚠️ Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Payment History & Delinquency Patterns Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How On-Time and Missed Payments Are Reported and Interpreted in Credit Scoring Models

Payment history is the most influential factor in most credit scoring models.

More than any other category, it reflects how accounts have been paid over time — and because of that, it often carries the greatest weight in how scoring models interpret credit data.

Many individuals review their credit report and notice late payments, delinquency entries, or negative marks and ask:

How much does this matter?

Why does one missed payment seem to have such a strong impact?

Why do older late payments still appear years later?

These questions are common because payment history is not evaluated as a single event — it is interpreted as a pattern of behavior over time.

This guide explains how on-time payments, missed payments, delinquency severity, frequency, recency, and long-term repayment patterns are reported and interpreted within scoring models such as FICO and VantageScore — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system explaining how credit data is interpreted across scoring models.

🧠 Who This Page Is For?

This page is designed for:

Individuals reviewing their credit report and seeing late payments or delinquency entries

People with past missed payments who want to understand how they are reported and interpreted

Anyone seeking factual, non-promotional explanations of how payment history appears in credit data

Those exploring credit scoring mechanics without repair claims or service-based solutions

This page provides educational context only — not recommendations or strategies.

📊 In This Guide

What payment history means in credit scoring

How payment history is reported

On-time payments vs delinquency

The Delinquency Impact Stack

The Payment History Timeline Effect

Frequency and recency of missed payments

Long-term payment patterns

Payment history in FICO and VantageScore models

How payment history interacts with other factors

Common observable patterns

Monitoring payment history

Frequently asked questions

📌 What Is Payment History in Credit Scoring?

Definition

Payment history is the record of whether payments on credit accounts have been made on time or late. It is the most heavily weighted factor in most credit scoring models.

Payment history reflects reported account performance over time, including:

On-time payments

Late payments

Missed payments

Collections

Charge-offs

👉 Key Insight:

Payment history is not a reflection of intent — it is a record of what was reported.

Featured Snippet:

Payment history is the record of whether payments on credit accounts have been made on time or late, and it is the most heavily weighted factor in most credit scoring models.

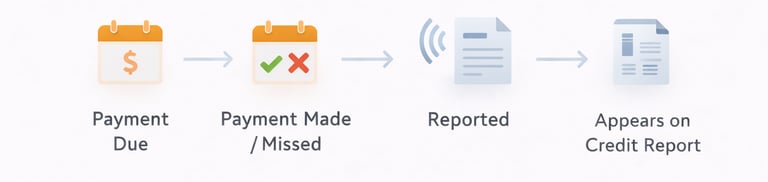

🔄 How Payment History Is Reported

Payment history is typically reported by creditors to the credit bureaus on a monthly cycle.

Reported data may include:

Payment due date

Payment received date

Account status

Days past due

Amount paid vs amount owed

Late payments are generally reported once an account becomes 30 days or more past due, with increasing levels of delinquency reported as time passes.

👉 This creates a timeline of account behavior that scoring models evaluate.

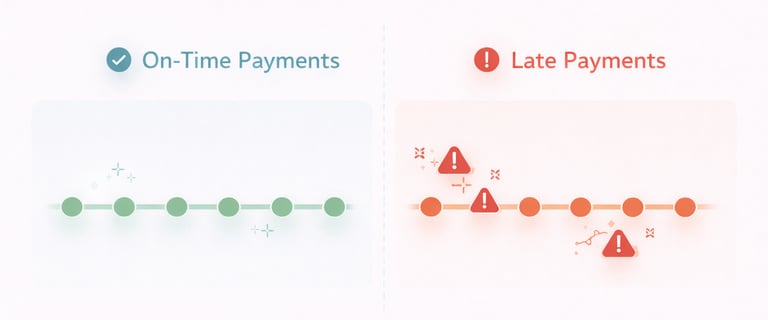

⚖️ On-Time Payments vs Delinquency

On-time payments are reported as current or paid as agreed.

Delinquency begins when a payment becomes late enough to be reported and is categorized by severity:

30 days late

60 days late

90 days late

120+ days late

As delinquency increases, it is typically interpreted differently within scoring models.

👉 A missed payment is not just an event — it becomes part of a longer behavioral record.

🧠 The Delinquency Impact Stack

Scoring models do not evaluate missed payments as isolated events.

Instead, they interpret a layered pattern of behavior that can be understood as:

1. Severity

How late the payment became

30 days late vs 90+ days late

Greater severity is often associated with stronger impact

2. Recency

How recently the delinquency occurred

Recent missed payments are typically more influential

Older delinquencies may carry less weight as they age

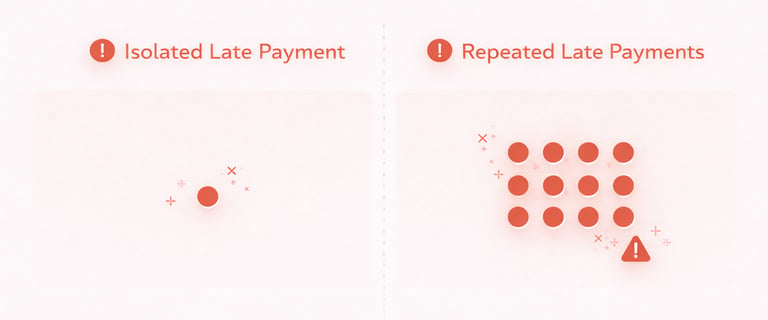

3. Frequency

How often payments were missed

A single late payment behaves differently than repeated delinquency

Multiple missed payments may indicate a broader pattern

4. Recovery Pattern

What happened after the delinquency

Did payments return to on-time status?

Did delinquency continue or escalate?

👉 Key Insight:

Scoring models are not asking, “Did you miss a payment?”

They are asking:

👉 “What pattern does this behavior create over time?”

📈 The Payment History Timeline Effect

Payment history is not evaluated as a single moment.

It is interpreted as a timeline of behavior, where:

Earlier activity establishes baseline reliability

Mid-history patterns reinforce consistency or instability

Recent activity carries stronger influence in interpretation

👉 Aha Moment:

A credit report is not a snapshot of one event — it is a timeline of reported behavior.

👉 Scoring models are not measuring perfection — they are measuring consistency across time.

⏳ Delinquency Severity Levels

Delinquency is typically reported in stages:

30 days late — first reportable level

60 days late — continued missed payments

90 days late — more significant delinquency

120+ days late — may lead to charge-off or collections

These levels are not treated equally. More severe delinquency is generally associated with stronger negative interpretation in model data.

Late payments and delinquency entries may remain on credit reports for up to 7 years from the date of first delinquency.

🔁 Frequency and Recency of Missed Payments

Scoring models evaluate patterns such as:

How many missed payments occurred

How recently they occurred

Whether behavior improved or worsened

Observed patterns often include:

Recent missed payments may carry stronger influence

Older missed payments may have reduced impact over time

Repeated delinquency may be interpreted differently than isolated events

👉 Key Insight:

Payment history is not about one mistake — it is about pattern consistency over time.

🧾 Long-Term Payment Patterns

Payment history is evaluated across the entire reported history of accounts.

Common long-term patterns include:

Consistent on-time payments over years often align with higher scores in model data

Repeated or escalating delinquency often corresponds to lower scores

Transition from delinquency back to on-time behavior may show gradual changes as data ages

👉 Scoring models are designed to interpret behavior across time — not just isolated events.

⚙️ Payment History in FICO and VantageScore Models

FICO Models

Payment history accounts for approximately 35% of the score

It is the most significant factor in commonly published FICO explanations

VantageScore 4.0

Payment history is weighted at approximately 41%

Greater emphasis on behavioral trends over time

Featured Snippet:

Payment history is the most important factor in most credit scoring models, accounting for about 35% in FICO and 41% in VantageScore.

🔗 How Payment History Interacts with Other Factors

Payment history does not operate independently.

It is interpreted alongside:

Credit utilization (balance behavior)

Negative items (collections, charge-offs)

New credit activity (recent applications and accounts)

Credit age (length of history)

Examples:

A missed payment + high utilization may amplify interpretation

A new account + delinquency may affect multiple scoring factors

Aging negative items may gradually change interpretation over time

👉 This interaction is explored further in:

📊 Common Observable Patterns

Across many credit profiles, commonly observed patterns include:

Long-term on-time payment history often associated with higher scores

Recent missed payments often associated with stronger impact

Isolated late payments may behave differently than repeated delinquency

Older negative entries may carry less influence as they age

These patterns reflect how scoring models interpret reported repayment behavior over time.

Monitoring Payment History Over Time

Some individuals choose to review their credit reports periodically to observe how payment history and delinquency status are reported over time.

Because payment history is based on reported data rather than real-time behavior, reviewing your credit profile can help connect what is happening in the system to what appears on your report.

For example, a late payment may appear differently depending on when it was reported, how severe it was, and whether later payments returned to current status. Observing these details directly can make it easier to understand how payment history is interpreted within scoring models.

Credit Monitoring Tool

Review your payment history, track account changes, and monitor how updates are reported over time

👉 View your credit profile here Affiliate Disclosure

This allows for the observation of reported data over time, but results may vary based on:

scoring model

credit bureau

timing of updates

🧠 Key Takeaway

Payment history is the most influential factor in most credit scoring models because it reflects behavior across time.

On-time payments, missed payments, severity, frequency, recency, and recovery patterns are all interpreted together as part of a broader behavioral timeline.

❓ Frequently Asked Questions (FAQ)

What is payment history in credit scoring?

Payment history is the record of whether payments on credit accounts have been made on time or late, and it is the most heavily weighted factor in most scoring models.

How is payment history reported?

Creditors report payment status to credit bureaus on a monthly cycle.

What is delinquency on a credit report?

Delinquency occurs when a payment becomes late enough to be reported, typically at 30+ days past due.

How long do late payments stay on a credit report?

Late payments generally remain for up to 7 years from the date of first delinquency.

How do late payments affect credit scores?

Late payments are often associated with lower scores, especially when recent or severe.

What is the difference between 30-day and 90-day late payments?

Severity is measured by days past due. A 90-day late payment is generally considered more severe than a 30-day late payment.

Can a single late payment affect a score?

A single late payment may be associated with score changes, though repeated or severe delinquency often has stronger impact.

Does consistent on-time history help offset older negative items?

Long-term on-time history may reduce the relative influence of older negative items as they age in model data.

← Previous Step: Credit Data Reporting & Structure

Next Step → Credit Utilization & Card Behavior

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT OFFER CREDIT REPAIR SERVICES, DISPUTE CREDIT REPORT ITEMS, OR PROVIDE ANY FORM OF CREDIT IMPROVEMENT ASSISTANCE. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion, Or consult a qualified professional.