Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Scoring Models Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Credit Scores Are Actually Calculated and Why Different Scores Exist

🧠 The Real Reason This Page Exists

Most people think they have “a credit score.”

They don’t.

What they actually have is:

👉 a result generated by a model

And that model is interpreting:

👉 a snapshot of reported data at a specific moment in time

That’s why:

Scores change when nothing “feels” different

Different apps show different numbers

The system can feel inconsistent

This page explains what’s actually happening behind the scenes — not as isolated facts, but as a system.

What This Page Is About

A credit score is not a thing you “have.”

It is something that is:

👉 calculated, interpreted, and recreated every time data changes

This page explains:

What a scoring model actually is

How scores are calculated

Why multiple scores exist

Why the same data produces different results

How models connect everything in the credit system

Who This Page Is For

People seeing different scores in different places

Anyone confused by Credit Karma vs Experian vs lender scores

Individuals trying to understand why scores change

Anyone who wants to understand how the system actually works

This is educational content only — no strategies or recommendations are provided.

🧠 What a Credit Scoring Model Actually Is

A credit scoring model is a system designed to analyze credit report data and estimate risk based on historical patterns.

It does not:

know you

understand intent

evaluate effort

It only sees:

👉 structured data and patterns over time

Simple Translation

A credit score is not a judgment.

It is:

👉 an output of a model interpreting data

Featured Snippet

A credit scoring model analyzes credit report data and produces a score based on patterns found in historical data, not personal judgment or individual intent.

🔍 The Most Important Concept (Most People Miss This)

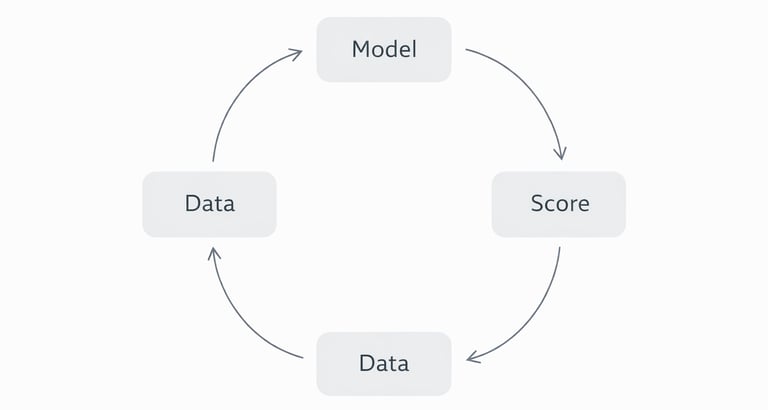

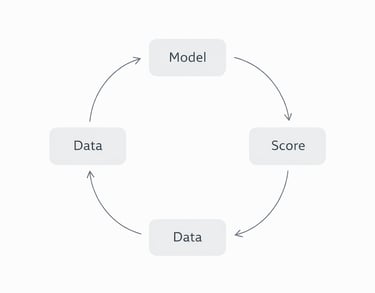

Scores do not “move” — they are recalculated

Every time new data is reported:

the model reviews the updated file

compares it to known patterns

generates a new score

👉 There is no memory of the previous score

👉 Only the current data snapshot matters

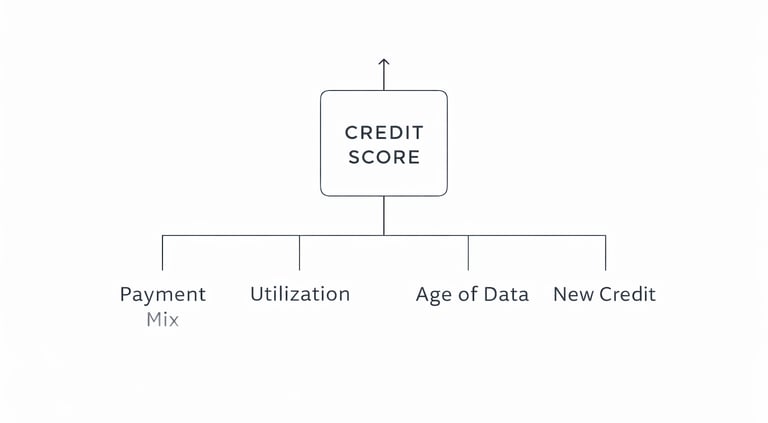

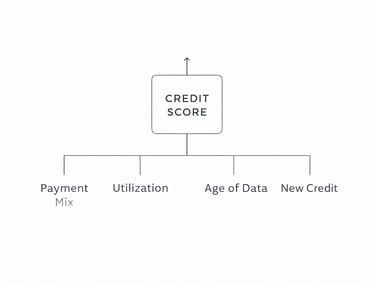

⚙️ How Credit Scores Are Built

Scoring models evaluate categories of data:

Payment history

Credit utilization

Credit age and file depth

Credit mix

New credit activity

Each category contributes differently depending on the model.

🧠 Why This Matters

No single action controls your score.

👉 Scores are the result of interactions between multiple data points

🔁 Why Different Credit Scoring Models Exist

There is no universal scoring system.

Different models exist because:

lenders have different risk tolerances

datasets differ

models evolve over time

The two most common systems are:

FICO

VantageScore

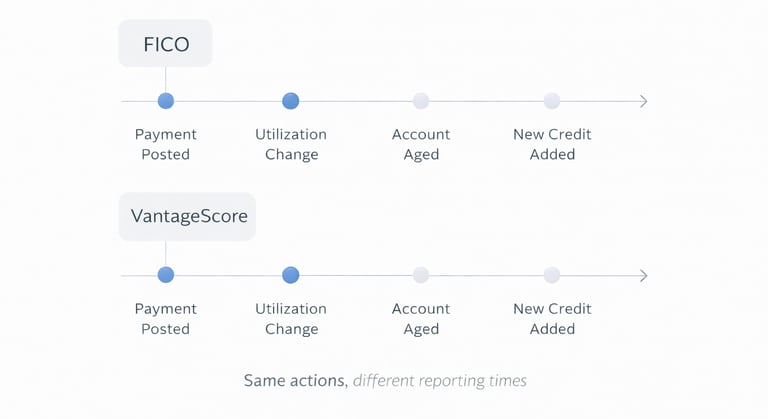

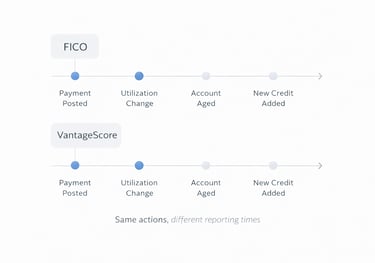

🔍 FICO vs VantageScore

FICO

Widely used by lenders

Heavily weighted toward payment history and utilization

Multiple versions exist for different industries

VantageScore

Often used in consumer tools

Responds more to recent trends

Updates faster with newer data

🧠 Key Insight

Both models look at:

👉 the same credit report

But they:

👉 interpret it differently

🤯 Why You Can Have Multiple Scores at the Same Time

You don’t have one score.

You have many.

Because scores depend on:

Model used

Bureau providing data

Timing of data updates

Example:

At the same moment, you can have:

Experian FICO score

TransUnion VantageScore

Lender-specific model score

👉 All different

👉 All valid within their system

🧠 Why the System Feels Inconsistent

This is where most people get stuck.

The system feels unpredictable because:

data updates at different times

multiple models interpret data differently

multiple factors change at once

🔥 Real Insight

What feels random is usually:

👉 timing + interaction between variables

Not chaos.

🔗 How Scoring Models Connect the Entire System

Scoring models sit on top of everything else.

They interpret:

Payment History → strongest signal

Utilization → current behavior

Age → historical depth

Mix → account diversity

New Credit → recent activity

Reported Data → structure and timing

👉 They don’t create data

👉 They translate it into a score

📊 Common Patterns Across Models

Across most scoring systems:

Consistent on-time payments align with stronger scores

High utilization often corresponds with lower scores

New accounts and inquiries may create temporary changes

Longer credit history stabilizes results

Multiple changes at once amplify movement

These are patterns — not guarantees.

🧠 Viewing and Comparing Credit Scores Across Models

Some individuals choose to observe how different scoring models interpret their credit data by using monitoring services that display multiple scores, data snapshots, and reporting updates over time.

Because credit scores are generated by different models — and based on data from different bureaus at different times — viewing multiple versions of a score can help illustrate how the same underlying information is interpreted in different ways.

For example, a single credit profile may produce different results depending on whether a model emphasizes recent trends, historical depth, or specific categories of data such as utilization or payment history.

Monitoring services allow individuals to observe:

How different scoring models evaluate the same credit data

How scores change as new information is reported

How timing, data sources, and model design influence results

One example of this type of service is IdentityIQ, which provides access to credit report data and model-based score outputs that can be reviewed over time.

Services like this do not determine credit outcomes or modify reported data. Instead, they provide a structured way to observe how credit information is presented and interpreted across different scoring environments.

Understanding how scores appear across models can help clarify why multiple scores exist at the same time and why those scores may differ — even when underlying behavior has not changed.

👉 For a deeper look at how monitoring services display credit data and track changes over time, continue to the Credit Monitoring & Credit Tools Framework.

Important Note

Different tools may show:

different models

different bureaus

different update timing

👉 That’s why scores vary.

🔥 Key Takeaway

A credit score is not a fixed number.

It is:

👉 a calculated result produced by a model interpreting reported data at a specific moment in time

Different models, different data, and different timing can all produce different scores — even when behavior is unchanged.

❓ Frequently Asked Questions

Why do I have multiple credit scores?

Because different scoring models, bureaus, and timing of data updates all produce separate results.

What is a credit scoring model in simple terms?

It’s a system that analyzes your credit data and calculates a score based on patterns in historical behavior.

Why do scores change even when I didn’t do anything?

Because data can update, age, or be interpreted differently — triggering a new calculation.

Is there one “real” credit score?

No. There are multiple valid scores depending on model, bureau, and timing.

Why do lenders use different scores than apps?

Lenders may use different versions of scoring models than consumer-facing tools.

Do all scoring models use the same data?

They use the same type of data, but may receive it from different bureaus and interpret it differently.

How often are scores calculated?

Every time new data is reported or updated, the score is recalculated.

← Previous Step: Credit Scoring Education Framework

Next Step → Credit Data Reporting & Structure

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT OFFER CREDIT REPAIR SERVICES, DISPUTE CREDIT REPORT ITEMS, OR PROVIDE ANY FORM OF CREDIT IMPROVEMENT ASSISTANCE. ACCURATE NEGATIVE INFORMATION CANNOT BE REMOVED FROM CREDIT REPORTS UNDER FEDERAL LAW. FOR QUESTIONS ABOUT YOUR PERSONAL CREDIT REPORT OR SCORE, CONTACT THE CREDIT BUREAUS (EQUIFAX, EXPERIAN, TRANSUNION) DIRECTLY OR CONSULT A QUALIFIED PROFESSIONAL.