Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Inquiries & New Credit Activity Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Inquiries and New Accounts Are Reported and Interpreted in Credit Scoring Models

Credit inquiries and new credit activity are part of what scoring models typically refer to as the “new credit” category. This category helps explain how recent applications and newly opened accounts are interpreted over time.

Many people notice new inquiries or accounts on their credit report after applying for credit and aren’t sure what they mean or how they’re evaluated. This guide explains how inquiries (both hard and soft) are recorded, how new accounts appear in your credit data, and how scoring models like FICO and VantageScore interpret this information — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system designed to explain how credit data is interpreted across scoring models.

Who This Page Is For?

This page is designed for:

Individuals who recently applied for credit and noticed inquiries on their report

People reviewing their credit report and seeing multiple inquiries or new accounts

New credit users learning how applications and accounts show up in credit data

Anyone looking for a clear, factual explanation of how inquiries and new credit activity are handled

This is an educational guide only — no strategies or recommendations are provided.

In This Guide

What are credit inquiries?

Hard inquiries vs. soft inquiries

How inquiries are reported

Inquiries vs. new accounts

New credit accounts and activity

How scoring models interpret inquiries and new credit

Common observable patterns

Rate shopping and multiple inquiries

How these factors change over time

Monitoring tools

Frequently asked questions

What Are Credit Inquiries?

Definition

A credit inquiry is a record showing when your credit report has been accessed.

There are two main types:

Hard inquiries (from credit applications)

Soft inquiries (for non-application purposes)

Inquiries are reported by the entity that accessed your credit report and may appear on your credit file.

Featured Snippet:

A credit inquiry is a record showing when a credit report is accessed, either as part of a credit application (hard inquiry) or for other purposes (soft inquiry).

Hard Inquiries vs. Soft Inquiries

Hard inquiries occur when a lender checks your credit as part of a credit application, such as:

Credit cards

Auto loans

Mortgages

Personal loans

Hard inquiries are visible to lenders and are generally used in credit

scoring models, where they may be associated with temporary changes in scores.

Soft inquiries occur for other reasons, including:

Checking your own credit

Pre-qualification offers

Background checks

Promotional reviews

Soft inquiries are not visible to lenders and are generally not used in scoring models.

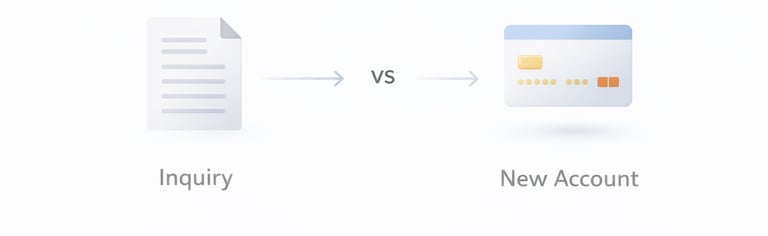

Inquiries vs. New Accounts

It’s important to separate these two concepts:

An inquiry means your credit report was accessed

A new account means credit was actually opened

Not every inquiry leads to a new account, but most new accounts are associated with a hard inquiry.

How Inquiries Are Reported

Hard inquiries are:

Visible on your credit report

Typically remain for up to 2 years

Often associated with score impact for a shorter period (commonly around 12 months in many models)

Soft inquiries:

Are not shown to lenders

Are not used in most scoring models

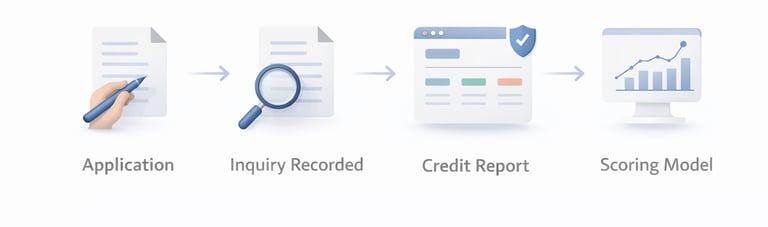

How Inquiry Data Flows Through Credit Reports

Application or credit check

→ Inquiry recorded

→ Appears on credit report

→ Evaluated within scoring models

This is how inquiry data moves through the system.

New Credit Accounts and Activity

New credit activity includes opening new accounts such as:

Credit cards

Loans

Lines of credit

When a new account is opened, it is reported to the credit bureaus and becomes part of your credit file.

Scoring models may evaluate:

How many new accounts you have

How recently they were opened

The type of credit added

Inquiries and New Credit in Scoring Models

In commonly published models:

FICO: New credit makes up about 10% of the score

VantageScore 4.0: Recent credit behavior is around 11%

Hard inquiries and new accounts are often associated with temporary changes in scores, especially when several occur within a short period.

Featured Snippet:

Hard inquiries may be associated with temporary lower scores in model data, while soft inquiries generally do not affect scores.

Rate Shopping and Multiple Inquiries

When shopping for certain loans (like mortgages or auto loans), multiple inquiries made within a short time may be treated as a single inquiry in many scoring models.

This is known as rate shopping.

This grouping behavior is designed to reflect comparison shopping

rather than multiple separate credit risks.

Common Observable Patterns

Based on historical model data, commonly observed patterns include:

Multiple inquiries in a short period may correspond with temporary score changes

A single inquiry often has minimal long-term impact

Several new accounts opened quickly may affect scores

Older inquiries (over ~12 months) tend to carry less influence

Individual results vary depending on the full credit profile.

How These Factors Change Over Time

Credit inquiries and new accounts evolve over time:

Hard inquiries remain visible for up to 2 years, but impact is often shorter

New accounts may initially reduce average account age

Over time, accounts may contribute to credit mix and history

👉 This connects directly to credit age, which is explored further in the Credit Age & File Depth guide

👁️ Viewing Inquiries and New Credit Activity in Your Profile

Credit inquiries and new accounts are recorded as part of your credit file and may appear differently depending on when applications were made, how accounts were opened, and how updates are reported by lenders.

Because these entries are tied to specific reporting timelines, reviewing your credit profile can help clarify how inquiries and new accounts are displayed and how they relate to the rest of your credit data.

For example, a hard inquiry may appear alongside a newly opened account, while multiple inquiries may be grouped differently depending on the type of credit and timing. Observing these details directly can help connect how new credit activity is recorded and interpreted within scoring models.

Credit Monitoring Tool

Review your credit report, including inquiries, new accounts, and reporting activity

👉 View your full credit profile and recent credit activity Affiliate disclosure

This will show reported data, but results may vary based on:

scoring model

credit bureau

update timing

Related Guides

👉 See the full system: Complete Credit Scoring Education Framework

👉 See how balances interact: Credit Utilization & Credit Card Behavior

👉 See how negative items fit in: Credit Report & Negative Items Framework

Key Takeaway

Credit inquiries and new accounts represent recent credit activity recorded in your credit file. While they may be associated with temporary changes in scores, they are just one part of a broader system used to evaluate credit data over time.

Frequently Asked Questions (FAQ)

What is a credit inquiry?

A record showing when your credit report was accessed.

What is a hard inquiry?

A credit check tied to a credit application.

What is a soft inquiry?

A credit check not related to an application.

Do hard inquiries affect scores?

They may be associated with temporary changes in scores.

Do soft inquiries affect scores?

No, they generally do not.

How long do inquiries stay on a report?

Up to 2 years, with shorter impact in most models.

What is rate shopping?

Multiple loan inquiries grouped as one within a short window.

Do new accounts affect scores?

They may initially affect scores due to account age and inquiries.

Are inquiries more impactful than negative items?

Negative items are generally associated with stronger impact.

← Previous Step: Credit Mix & Account Types

Next Step → Credit Report & Negative Items

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com does not: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion Or consult a qualified professional. See Full Disclaimer