Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Report & Negative Items Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Negative Information Is Reported, Retained, and Interpreted in Credit Reports

Negative items are one part of the broader credit scoring system, primarily

within the payment history category, which is the most heavily weighted

factor in most credit scoring models.

Many individuals review their credit report and see negative entries — late payments, collections, charge-offs, or other derogatory marks — that remain visible even after years. This can feel confusing, especially when current financial behavior has improved.

This guide explains how negative information is reported, how long it typically remains on credit reports, how it is interpreted within scoring models, and how it fits into the broader credit data system — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system explaining how credit data is interpreted across scoring models.

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

🧠 Who This Page Is For

This page is designed for:

Individuals reviewing their credit report and seeing negative items or derogatory marks

People with past late payments, collections, or charge-offs who want to understand reporting timelines

Anyone seeking factual, non-promotional explanations of how negative information appears in credit reports

Those exploring credit data without repair claims or service-based solutions

This page provides educational context only, not recommendations or strategies.

📊 In This Guide

What are negative items on a credit report?

How negative information is reported

Common types of negative items

Reporting timelines

How negative items are interpreted in scoring models

How negative items change over time

Observable patterns in credit data

Why negative items remain on reports

Monitoring negative items

Frequently asked questions

📌 What Are Negative Items on a Credit Report?

Definition

Negative items are entries on a credit report that reflect missed or late payments, defaults, collections, charge-offs, bankruptcies, or other derogatory marks reported by creditors, collection agencies, or public records.

Seeing a negative item does not necessarily reflect current financial behavior — it reflects how an account was reported at a specific point in time.

Featured Snippet:

A negative item on a credit report is an entry such as a late payment,

collection, charge-off, or bankruptcy that reflects past account activity

reported to credit bureaus.

🔄 How Negative Information Is Reported

Negative information is reported to credit bureaus by:

Creditors (late or missed payments)

Collection agencies (accounts sent to collections)

Public records (bankruptcies and certain legal filings)

Reporting is governed by the Fair Credit Reporting Act (FCRA), which establishes rules for:

Accuracy

Timeliness

Consumer rights

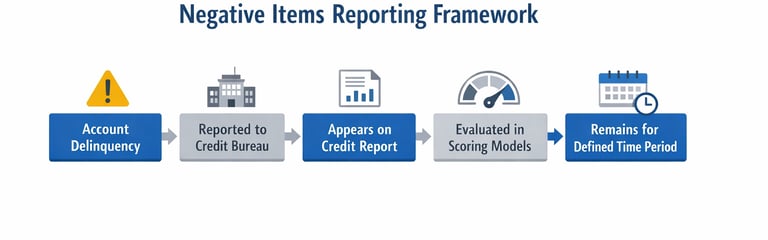

🔍 How Negative Items Appear in Credit Reports

Delinquency → Reported to Credit Bureau → Appears on Credit Report → Evaluated in Scoring Models

📉 Common Types of Negative Items

Late payments (30+ days past due)

Collections

Charge-offs

Bankruptcies (Chapter 7 and Chapter 13)

Foreclosures and repossessions

Other derogatory account statuses

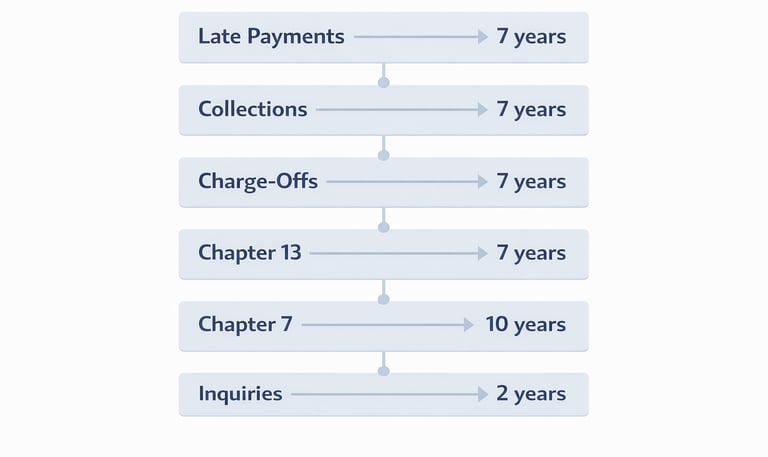

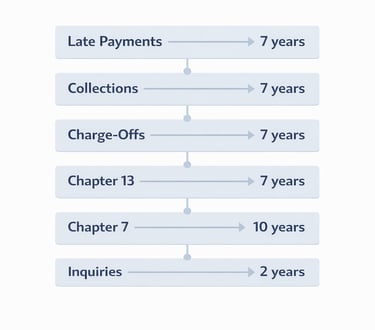

⏳ Reporting Timelines for Negative Information

The Fair Credit Reporting Act (FCRA) sets general guidelines for how long different types of negative information may remain on a credit report.

These timeframes typically include:

Late payments – generally remain for up to 7 years from the date of first delinquency

Collections – typically remain for up to 7 years from the original delinquency date on

the account

Charge-offs – usually remain for up to 7 years from the date of first delinquency

Chapter 13 bankruptcy – may remain for up to 7 years from the filing date

Chapter 7 bankruptcy – may remain for up to 10 years from the filing date

Hard inquiries – may remain on the report for up to 2 years, though their impact on scoring models is often shorter (commonly around 12 months)

These are generally considered maximum reporting periods under federal law.

Some items may be removed earlier depending on reporting accuracy or verification.

👉 These timelines are based on federal reporting standards and apply across most credit reporting scenarios.

🧠 How Negative Items Are Interpreted in Scoring Models

Negative items are evaluated primarily within payment history, the most influential factor in credit scoring models.

FICO models: ~35%

VantageScore models: ~41%

Negative items are typically more influential when they are:

Recent

Severe

Repeated

👉 See how this connects to balances in our Credit Utilization & Credit Card Behavior guide

👉 Learn how timing affects scoring in Payment History & Delinquency Patterns

📊 How Negative Items Change Over Time

Negative items are not static in their impact.

Observed patterns include:

Stronger impact when recent

Gradually reduced influence as they age

Continued visibility for the full reporting period

Scoring models evaluate patterns over time, not just single events.

📉 Common Observable Patterns

Multiple negative items across accounts are often associated with lower scores

Recent derogatory marks may have stronger impact

Older items may carry less influence

Isolated late payments may behave differently than ongoing delinquencies

🧾 Why Negative Items Remain on Credit Reports

Negative items remain because:

Credit scoring systems rely on historical data patterns

Lenders evaluate long-term repayment behavior

The FCRA establishes standardized reporting timelines

🔗 How Negative Items Fit Into the Bigger Credit System

Negative items are evaluated alongside:

Credit utilization

Credit age

Credit mix

Recent activity

👉 See the full system in the Complete Credit Scoring Education Framework

👁️ Viewing Negative Items in Your Credit Report

Negative items are reported as part of your credit file and may appear differently depending on how accounts were reported, when updates occurred, and which bureau is providing the data.

Because these entries are tied to specific reporting timelines and account histories, reviewing your own credit report can provide a clearer picture of how negative items are displayed and how they relate to the rest of your credit profile.

For example, a collection account, charge-off, or late payment may appear with different dates, statuses, or updates depending on how the information is reported and maintained over time.

Observing these details directly can help connect how negative items are recorded, how long they remain visible, and how they fit into the broader credit data system.

Credit Monitoring Tool

Review your credit report, including negative items, account status, and reporting timelines

👉 View your full credit profile and negative items Affiliate disclosure

🧠 Key Takeaway

Negative items represent historical credit activity recorded over time. While their impact may change as they age, they remain part of the broader dataset used by credit scoring models.

❓ Frequently Asked Questions (FAQ)

What are negative items on a credit report?

Negative items are entries such as late payments, collections, charge-offs, or bankruptcies that reflect past account activity reported to credit bureaus.

How long do late payments stay on a credit report?

Late payments generally remain for 7 years from the date of first delinquency.

How long do collections stay on a credit report?

Collections typically remain for 7 years from the original delinquency date.

How long do charge-offs stay on a credit report?

Charge-offs generally remain for 7 years from the date of first delinquency.

How long does bankruptcy stay on a credit report?

Chapter 7 may remain up to 10 years, while Chapter 13 may remain up to 7 years.

Do negative items get removed earlier?

Negative items may be removed earlier if they are inaccurate, unverifiable, or reach the end of the reporting period.

Do paid collections disappear?

Paid collections may still remain on the report, but are typically shown as paid.

Do medical collections follow the same rules?

Some medical collections may have additional reporting considerations, but general timelines still apply.

How do negative items affect credit scores?

Negative items are often associated with lower scores, especially when recent or severe.

Can negative items be disputed?

Consumers have the right to dispute inaccurate or incomplete information under the Fair Credit Reporting Act.

← Previous Step: Credit Inquiries & New Credit Activity

Next Step → Credit Score Changes & Fluctuations

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com DOES NOT: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion Or consult a qualified professional.