Follow the Credit System Step-by-Step

Educational content only. Not credit repair advice or services. No guarantees made. See full Disclaimer

Credit Score Changes & Fluctuations Framework

This page is part of the Credit Patterns Framework — a step-by-step system designed to explain how credit scores are calculated, interpreted, and updated over time.

How Credit Scores Are Dynamic and What Influences Reported Fluctuations

Credit scores are not fixed numbers.

Many people notice their score changing from one month to the next — sometimes even when nothing obvious has changed. You might see a drop, an increase, or just small fluctuations and wonder what caused it.

This guide explains how credit scores change over time, what reported data influences those changes, and how scoring models interpret updates — without offering advice, services, or guarantees.

This page is part of the CreditPatterns.com Credit Education Framework, a structured system designed to explain how credit data is interpreted across scoring models.

🧠 Who This Page Is For?

This page is designed for:

Individuals who notice their credit score changed unexpectedly

People reviewing score updates and wondering what caused the change

Anyone tracking their credit data over time

Individuals seeking clear, factual explanations of score fluctuations

This is an educational guide only — no strategies or recommendations are provided.

📊 In This Guide

Why credit scores are dynamic

How scoring models recalculate scores

Reporting cycles and score updates

Common causes of score fluctuations

Expected vs unexpected changes

How different factors interact

Differences between scoring models

Common fluctuation patterns

Why timing creates confusion

Monitoring score changes

Frequently asked questions

Why Credit Scores Are Dynamic

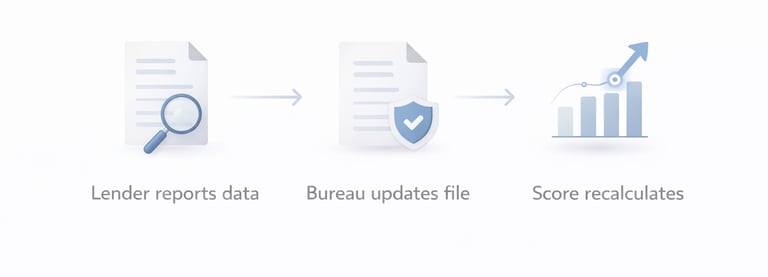

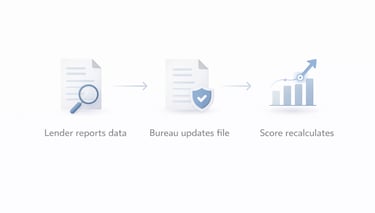

Credit scores are recalculated whenever new or updated information is reported to the credit bureaus.

Because credit reports are constantly changing — balances, payments, new accounts, and other updates — scores also change.

Scores do not update continuously in real time.

They update when new data is reported.

Featured Snippet:

Credit scores can change when new information is reported to credit bureaus, such as updated balances, payments, or new accounts.

How Scoring Models Recalculate Scores

Each time new data is reported, scoring models take a new snapshot of your credit file.

They do not gradually adjust your score.

Instead:

A new snapshot of your credit data is created

That snapshot is evaluated using the scoring model

A completely new score is generated

🧠 Key Point

Credit scores do not “move up or down” on their own.

Each change reflects a new calculation based on updated data.

Reporting Cycles and Score Updates

Most lenders report account information to credit bureaus on a monthly basis.

Because of this:

A payment made today may not appear for 30–60 days

A balance reduction may not show until the next reporting cycle

New accounts or inquiries may appear sooner

This delay is one of the most common reasons score changes feel confusing.

Common Causes of Credit Score Fluctuations

Score changes are usually tied to updates in reported data.

Common causes include:

Changes in credit utilization (balances or limits)

New accounts or credit inquiries

Late payments or other negative items

Aging of accounts or negative items

Corrections or updates to reported information

Often, multiple updates happen at the same time — for example:

👉 A balance increase + a new inquiry + a new account

Expected vs Unexpected Score Changes

Some changes are expected:

Normal spending or balance changes

Opening a new account

Payments being reported

Other changes may feel unexpected:

Timing differences in reporting

Reporting delays or inconsistencies

Differences between credit bureaus or scoring models

This helps explain why scores can change even when behavior stays the same.

How Different Factors Work Together

Credit scores reflect multiple factors interacting at once.

Examples:

A balance increase raises utilization → often associated with lower scores

A new inquiry and new account → affects both new credit and account age

A late payment combined with high utilization → stronger combined impact

👉 See related topic: Credit Utilization & Credit Card Behavior

👉 See related topic: Credit Report & Negative Items Framework

Differences Between Scoring Models

Different scoring models interpret changes differently.

FICO models

Focus on specific data updates like utilization, payment history, and new credit

VantageScore models

Place more emphasis on trends over time

Because of this, the same credit data can produce different score changes depending on the model used.

Common Observable Patterns

Based on historical model data:

Scores may decrease after higher utilization is reported

Scores may change after new inquiries or accounts

Temporary fluctuations can occur around payment timing

Scores may gradually improve as negative items age

These are commonly observed patterns — not guaranteed outcomes.

Why Timing Creates Confusion

Timing plays a major role in score fluctuations.

Reporting is not real-time

Different bureaus update at different times

Statement dates affect reported balances

Payments may post after reporting

This can create short-term changes that don’t reflect long-term behavior.

How Data Changes Translate Into Score Changes

Here’s how common changes typically appear:

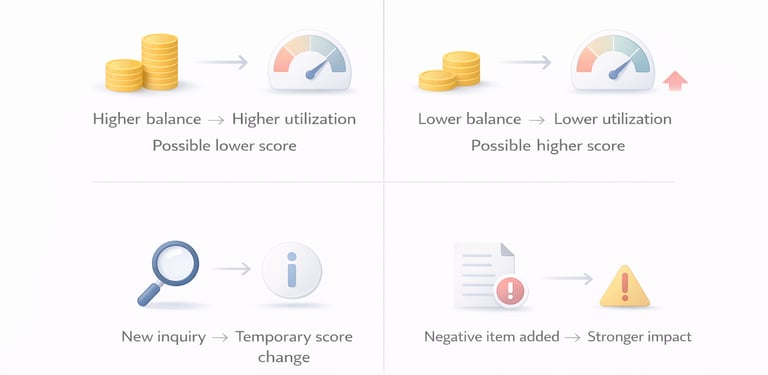

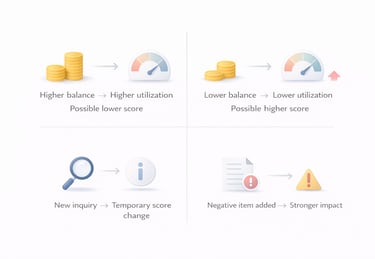

When balances increase → utilization rises → often associated with lower scores

When balances decrease → utilization drops → often associated with higher scores

When a hard inquiry is added → temporary change may occur

When a new account is opened → average account age may decrease and multiple factors may be affected

When a negative item is added → payment history is impacted → often stronger effect

When a negative item ages → its impact may gradually decrease over time

These examples illustrate how scoring models interpret data — not direct cause-and-effect rules.

👁️ Tracking Credit Score Changes Over Time

Credit scores do not change randomly. They are recalculated based on updated data, which means even small changes in balances, payment timing, account activity, or reporting cycles can result in different outcomes.

Because multiple factors often change at the same time, it can be difficult to isolate what caused a specific score movement without viewing how data is updating across your full credit profile.

For example, a score change may reflect a combination of utilization updates, new account activity, or aging data — all interacting within the same reporting cycle.

Observing these changes over time can help reveal patterns in how scoring models respond to different types of updates rather than focusing on a single event.

Credit Monitoring Tool (Advanced Tracking)

Track score changes, account updates, and reporting patterns over time

👉 Track your credit changes and score behavior over time Affiliate Disclosure

This tool allow individuals to observe reported data and score changes over time.

However, results may vary depending on:

The scoring model used

The credit bureau providing the data

The timing of updates

👉 Learn more: Credit Monitoring & Credit Tools

👉 Related: Credit Utilization & Credit Card Behavior

👉 Related: Credit Report & Negative Items Framework

🧠 Key Takeaway

Credit scores are dynamic.

They reflect the most recent snapshot of your credit report — not a fixed number.

Fluctuations occur when new or updated data is processed, and each change represents a new calculation based on that data.

❓ Frequently Asked Questions

Why did my credit score change?

Scores can change when new information is reported, such as balances, payments, inquiries, or new accounts.

How often do credit scores change?

They can change whenever new data is reported, typically on a monthly cycle.

Why did my score drop even though I paid on time?

Changes may be related to utilization, new accounts, inquiries, or other reported updates.

Why did my score go up suddenly?

Increases may be associated with lower utilization or aging of negative items.

What causes monthly fluctuations?

Monthly updates, reporting cycles, and timing differences.

Does paying off a credit card change my score?

Lower balances may reduce utilization, which is often associated with score changes when reported.

How long does it take for a payment to affect my score?

Typically after the next reporting cycle (about 30–45 days).

Can a score change without new activity?

Yes — due to aging accounts, data updates, or corrections.

Are credit score fluctuations normal?

Yes — fluctuations are a normal part of how scoring models process updated data.

← Previous Step: Credit Report & Negative Items

Next Step → Credit Monitoring & Tools

🔗 Explore the Credit Education Framework

This page is part of a connected system of educational resources:

Each section explains one component of how credit scoring models interpret real-world credit data.

⚠️ Final Disclaimer

THIS ARTICLE IS PROVIDED FOR GENERAL EDUCATIONAL PURPOSES ONLY AND IS NOT CREDIT REPAIR ADVICE, CREDIT REPAIR SERVICES, FINANCIAL ADVICE, OR PERSONALIZED GUIDANCE. CreditPatterns.com does not: Offer credit repair services, Dispute credit report items, Provide credit improvement assistance. Accurate negative information cannot be removed from credit reports under federal law. For questions about your credit report, contact: Equifax, Experian, TransUnion Or consult a qualified professional.