Follow the Credit System Step-by-Step

Why Your Credit Score Changes: The Complete Pattern-Based Explanation (Drops, Increases & Timing)

Why does your credit score change? Learn the real reasons for drops and increases, how reporting timing and utilization work, and how credit patterns drive your score.

CreditPatterns.com

3/23/20264 min read

Why does your credit score change?

Your credit score changes because lenders report updated information about your balances, payments, and account activity. Credit scoring models evaluate patterns over time—not just single actions—so changes in utilization, timing, or account behavior can cause your score to rise or fall.

To understand how these changes actually work at a system level, it helps to look at the full Credit Scoring Framework and how different factors connect over time.

🧠 INTRO

Most explanations about credit scores are technically correct—but practically useless.

You’ll hear things like:

“Payment history matters”

“Keep your balances low”

“Don’t open too many accounts”

But that doesn’t answer the real question:

👉 Why did your score change this week, even when you didn’t do anything different?

The answer is not in the factors.

👉 It’s in the pattern those factors create over time.

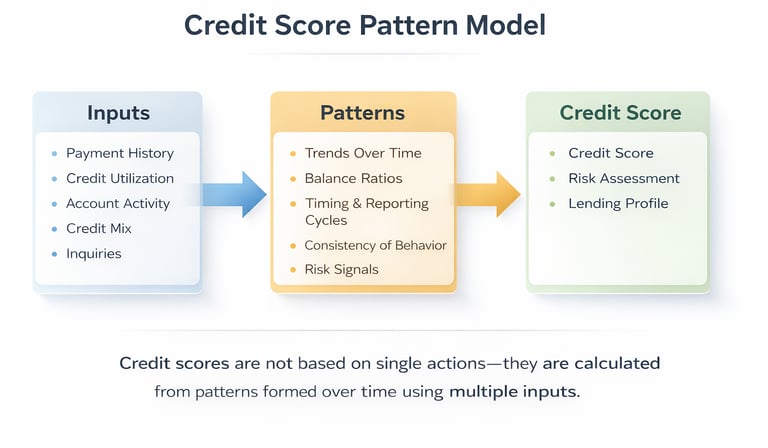

🔥 THE CORE MODEL

How Credit Scores Actually Work

At a high level, every credit score follows this structure:

Inputs → Patterns → Score

Inputs = balances, payments, accounts

Patterns = trends, ratios, timing

Score = interpretation of risk

Most people focus on inputs.

👉 Scoring models focus on patterns.

This distinction explains nearly every “mysterious” credit score change.

🔥 SECTION: THE 5 REAL DRIVERS OF SCORE CHANGES

1. Credit Utilization (Real-Time Sensitivity)

Credit utilization measures how much of your available credit is being used.

But here’s the nuance:

👉 It is evaluated based on reported balances, not your intentions.

Changes in balances are one of the most common drivers of score movement, especially when viewed through the lens of credit utilization behavior and how it is reported.

If your balance is reported high—even temporarily—your score may drop.

The Consumer Financial Protection Bureau identifies credit usage patterns as a major factor in credit evaluation.

2. Reporting Timing (The Hidden Variable)

This is where most confusion comes from.

Your lenders report at different times:

statement closing date

reporting cycles

processing delays

So:

👉 You can pay everything on time

👉 And still see a drop

Much of this confusion comes from how data is captured and reported within the credit system itself, which is explained in more detail in the credit report structure framework.

Because your score is reacting to when data is captured—not when you acted

3. Payment Consistency (Not Just Payment History)

Payment history is not just about being “on time.”

It’s about:

👉 consistency over time

Payment consistency plays a critical role in long-term scoring patterns, particularly within the broader context of payment history and delinquency patterns.

According to FICO, long-term reliability is one of the strongest indicators of creditworthiness.

4. New Credit Activity (Profile Shifts)

Opening accounts or applying for credit changes how your profile is interpreted.

New applications and inquiries can temporarily shift your profile, which is part of the broader credit inquiries and new credit activity framework.

Even responsible behavior can:

temporarily lower your score

shift your risk profile

reset certain pattern metrics

5. Profile Composition (Structure Matters)

Your mix of accounts—cards, loans, etc.—affects how your profile is evaluated.

But again:

👉 It’s not the mix itself

👉 It’s the pattern of how that mix behaves over time

Why did my credit score drop for no reason?

Your credit score did not drop for no reason. It likely changed due to updated reported balances, timing differences in reporting, or shifts in your overall credit usage patterns—even if your behavior did not change significantly.

🔥 SECTION: WHY SCORES FEEL RANDOM (BUT AREN’T)

This is the most misunderstood part of credit scoring.

Your score is not a real-time reflection.

It is a:

👉 lagging indicator of reported behavior

That means:

today’s score may reflect last month’s balances

recent payments may not be reflected yet

temporary spikes can create temporary drops

This creates the illusion of randomness.

🔥 SECTION: WHY YOUR SCORE GOES UP

Score increases happen when patterns improve:

lower utilization

consistent payments

aging accounts

reduced negative impact

These changes don’t always happen immediately.

👉 They accumulate and then reflect.

🔥 SECTION: THE SHIFT THAT CHANGES EVERYTHING

Stop Thinking in Events. Start Thinking in Patterns.

Most people ask:

❌ “What did I do wrong?”

The better question is:

✅ “What pattern changed?”

This includes:

balance trends

timing relationships

account interactions

Once you think this way:

👉 credit scores become predictable

These concepts are part of a larger system that connects all aspects of your credit profile together, which you can explore in the full credit scoring education framework.

🔥 PRACTICAL APPLICATION

How to Understand Your Own Score

To actually interpret your score:

Look at:

your reported balances (not just payments)

timing of statements

recent activity

overall trend direction

Not isolated events.

Seeing Credit Patterns in Real Time

Understanding how credit scoring works conceptually is valuable.

But seeing how these patterns appear in your own profile is what creates clarity.

Tools that track your credit data over time can help you observe these changes as they happen—making it easier to connect what you’re learning to real outcomes.

👉 Start here to understand the full system: Credit Scoring Framework

🔥 HIGH-INTENT SECTION

What To Do Next

Once you understand how credit scores actually change, the next step is using that knowledge to evaluate your options.

Some platforms allow you to:

compare financial options

see what you qualify for

explore choices without impacting your score

🔥 FAQ

What causes credit score changes?

Credit score changes are caused by updates to reported balances, payment activity, credit utilization, and overall behavior patterns over time.

Why does my credit score change every month?

Because lenders report new data regularly, and scoring models adjust based on updated patterns in your credit profile.

Why did my credit score drop even though I paid on time?

Because your score reflects reported balances and timing—not just payment behavior—so reporting cycles can temporarily affect your score.

Is it normal for credit scores to fluctuate?

Yes. Small increases and decreases are normal and reflect updates to your credit profile.

🔗 Understand the Full System

If you want to see how all of these patterns connect, start here:

👉 Credit Scoring Framework

👉 Start Here: Credit Scoring Education Framework