Follow the Credit System Step-by-Step

How Credit Utilization Affects Your Credit Score (And Why It Changes Even When You Pay On Time)

Credit utilization drives up to 30% of your credit score, yet it’s one of the most misunderstood factors. Learn why your score can drop after paying on time, how reporting timing affects your data, and how to control utilization for stronger, more consistent credit performance.

CreditPatterns.com

3/27/20268 min read

You paid your credit card balance in full and on time. No missed payments. No new spending. Yet when you checked your score, it stayed flat—or worse, it dropped 10 to 30 points.

This scenario plays out for millions of responsible consumers every month and ranks among the most frustrating experiences in personal finance.

The culprit is almost always credit utilization, a factor that accounts for about 30% of your FICO score and around 20% of a VantageScore. It ranks as one of the most influential and fastest-moving elements in modern scoring models outlined in the Credit Scoring Models Framework.

Unlike Payment History & Delinquency Patterns, which evaluates your past reliability, utilization reflects your current borrowing patterns—but only through the narrow lens of what lenders actually report to the bureaus. This “reported reality” gap often creates a disconnect between your real-world actions and the number that appears on your credit report.

🔍 What Percentage of Your Credit Score Is Utilization? Credit utilization typically accounts for about 30% of a FICO score and around 20% of a VantageScore, making it one of the most influential factors in credit scoring models.

What Is Credit Utilization?

Credit utilization ratio measures how much of your available revolving credit—primarily credit cards and other lines of credit—you are actively using. The basic formula is straightforward:

Total reported revolving balances ÷ Total revolving credit limits × 100

Scoring models don’t stop at a single overall percentage. They evaluate three interconnected layers as part of broader Credit Utilization & Credit Card Behavior:

Overall utilization across every revolving account in your file.

Individual (per-card) utilization on each separate account.

Balance distribution, or how evenly (or unevenly) your balances spread across multiple cards.

FICO folds utilization heavily into its “amounts owed” category, which carries a 30% weight in classic models. VantageScore treats credit usage similarly but breaks it down further and places greater emphasis on trended patterns in versions like VantageScore 4.0.

Real-World Example Imagine you carry three credit cards with a combined total credit limit of $30,000 and current reported balances of $9,000. Your overall utilization sits at 30%. After making a sizable payment that brings balances down to $3,000, your utilization falls to 10%. The math is simple, yet your credit score may not reflect that improvement right away—especially if the payment falls after the reporting snapshot.

Why Your Score Can Drop After Paying On Time (The Timing Trap)

Credit card issuers rarely report balances in real time. Instead, they send monthly snapshots to Equifax, Experian, and TransUnion, most often tied to your statement closing date rather than your payment due date. This reporting timing dynamic explained in the Credit Data Reporting & Structure Framework sits at the heart of many unexpected score movements explained in the Credit Score Changes & Fluctuations Framework and ties directly into how data flows in the Credit Report & Negative Items ecosystem.

Here’s how it typically unfolds:

You make a large payment mid-cycle, say on the 20th.

Your issuer’s reporting cutoff occurred on the 15th, capturing the higher statement balance from earlier in the month.

The next time a lender or scoring model pulls your report, it still sees the elevated utilization from the prior snapshot.

As a result, your score reflects yesterday’s data, not today’s lower reality. Most consumers see the positive shift appear within the next 30–45 days once all issuers update their reports. Until then, the lag can feel arbitrary and discouraging.

Why Your Score Feels “Wrong”

Your ActionSystem SnapshotScore ResultPay BalancePrevious BalanceNo Change or Drop

This mismatch is the result of reporting timing, not scoring errors.

Other frequent triggers for utilization-related drops—even with perfect payment behavior—include:

Paying off a card in full and then closing the account, which shrinks your total available credit and spikes the ratio on remaining cards (affecting Credit Mix & Account Types).

Issuer-initiated credit limit reductions (sometimes triggered by broader economic conditions or your spending patterns).

Asynchronous reporting across multiple accounts, where one card updates with a high balance while others lag.

These mechanics explain why credit can feel unpredictable even when your financial habits remain rock-solid.

🔍 What Happens If Your Credit Utilization Is Too High? High credit utilization signals increased borrowing risk and is often associated with lower credit scores, especially when balances exceed 30% of available credit.

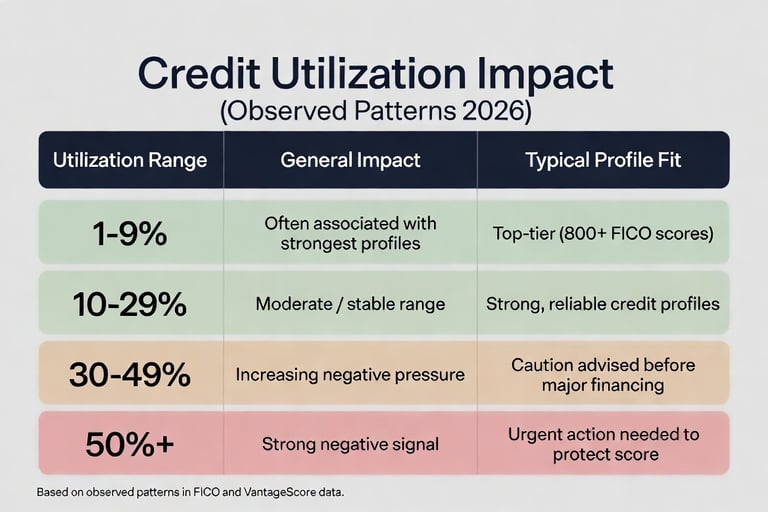

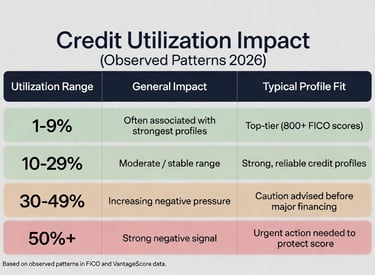

How Much Utilization Is “Good”? Data-Backed Guidelines for 2026

No universal magic number exists, but clear statistical patterns emerge from FICO, Experian, VantageScore, and consumer data as of early 2026. Consumers with exceptional FICO scores (800+) typically maintain overall and per-card utilization in the single digits—often averaging around 6.5% to 7.1%. The national average hovers closer to 29–36% depending on the quarter and economic conditions, with lower ratios strongly correlated to higher scores. Those with perfect 850 FICO scores often average just 4% utilization on credit cards.

Here is a practical breakdown based on observed patterns:

Credit Utilization Impact (Observed Patterns)

Lower utilization consistently correlates with better outcomes because it demonstrates to lenders that you manage credit responsibly and are not overextended. This relationship is one of the most consistently observed patterns across modern credit scoring datasets.

However, maintaining absolute 0% utilization long-term across all cards is not ideal either. It can signal a lack of active, responsible usage to some models, providing fewer positive data points about your credit behavior. A low but consistent 1–9% range often performs slightly better for active credit files, especially when viewed through Credit Age & File Depth.

Newer scoring models, including FICO 10T and VantageScore 4.0, incorporate trended data that examine utilization patterns over 12–24 months rather than single monthly snapshots. This shift rewards sustained low utilization and penalizes volatile swings more effectively than older models.

Why Utilization Has Such a Strong Impact

Utilization stands out because it offers lenders a current window into borrowing behavior. While Payment History & Delinquency Patterns (35% of FICO) looks backward at reliability, utilization shows what is happening right now in the reported data. This forward-looking signal helps predict risk, which is why it carries substantial weight in scoring models outlined in the Credit Scoring Models Framework.

“Credit is a system built on trust, and trust is built on consistency over time.” — Adapted from classical credit risk theory.

High utilization, even with on-time payments, can suggest potential financial strain or over-reliance on credit. Conversely, consistently low utilization reinforces a picture of disciplined money management and interacts with other elements like Credit Inquiries & New Credit Activity.

🔍 Does Credit Utilization Affect Your Score Quickly? Yes. Credit utilization is one of the fastest-changing factors in credit scoring because it is based on recently reported balances rather than long-term history.

Proven Strategies to Optimize Utilization in 2026

Mastering utilization requires proactive habits rather than reactive fixes. Here are detailed, actionable steps tailored to today’s reporting environment, all supported by sound Credit Utilization & Credit Card Behavior principles:

Master Your Reporting Cycles Log into each credit card account and note the exact statement closing date (typically 21–25 days before the due date). Make extra or full payments several days before this cutoff to ensure the lower balance gets captured in the next report.

Pay More Frequently Instead of waiting for one large end-of-month payment, spread smaller payments throughout the billing cycle. This keeps reported balances lower on average and reduces the chance of a high snapshot.

Request Strategic Credit Limit Increases A higher limit lowers your utilization ratio automatically—if you avoid increasing spending proportionally. Time these requests carefully, ideally when your income and payment history support them, and steer clear of periods with upcoming hard inquiries.

Distribute Balances Wisely Keep individual card utilization low, even when overall utilization looks moderate. Maxing out even one card sends a stronger negative signal than evenly spread moderate balances.

Avoid Common Pitfalls Resist the urge to close paid-off cards unless absolutely necessary, as this reduces total available credit and can temporarily inflate utilization while affecting Credit Mix & Account Types and Credit Age & File Depth. Monitor for unexpected limit decreases from issuers.

Leverage Monitoring Tools Use free or low-cost platforms to track reported (not just current) balances weekly. This visibility helps you spot patterns before they affect your score—see our guide to Credit Monitoring & Credit Tools for recommended options.

Pro Tip for Major Life Events: If you plan to apply for a mortgage, auto loan, or other significant financing, begin lowering utilization 60–90 days in advance. Trended models increasingly reward consistent low patterns over short-term drops.

Utilization never operates in isolation. It interacts dynamically with Payment History & Delinquency Patterns, length of credit history, Credit Mix & Account Types, new credit activity, and broader score movements explained in the Credit Score Changes & Fluctuations Framework.

🔍 Does Paying Off a Credit Card Immediately Improve Your Score? Not immediately. Credit scores update based on reported balances, so improvements are typically reflected after the next reporting cycle.

The Bigger Picture: Utilization in the Full Credit System

To truly control your credit, zoom out and view utilization as one piece of a larger ecosystem within the Complete Credit Scoring Education Framework. It connects directly to how data flows through the bureaus , and how scores evolve over time.

In practice, small, consistent improvements in utilization can compound. A consumer who reduces utilization from 35% to 8% over several months while maintaining perfect payments often sees gains of 20–60 points, depending on their starting profile and the specific model used.

Key Takeaways

Credit utilization is fundamentally about reported snapshots, not your current bank balance or good intentions.

Timing of payments relative to reporting dates explains the majority of post-payment score drops or stalls.

Aim for under 10–30% overall and per card, with single digits ideal for elite profiles. Consistency over multiple cycles matters more than any single month’s perfection.

With trended data gaining prominence in 2026 models, sustained low utilization delivers the strongest long-term rewards.

Mastering this factor won’t just stabilize your score—it positions you as a lower-risk borrower in the eyes of lenders, potentially unlocking better interest rates, higher limits, and greater financial flexibility.

Observing your utilization across multiple reporting cycles reveals patterns that are not visible in a single snapshot. When you begin to track how balances are reported—not just how they are paid—you shift from reacting to score changes to understanding and influencing them with precision.

FAQ: Credit Utilization Questions Answered

What is a good credit utilization ratio? Under 30% is generally solid for good credit; under 10% is ideal for excellent scores. Top-performing profiles often maintain single-digit ratios.

Why did my credit score drop after paying my credit card? The payment most likely posted after your issuer’s reporting date. The updated lower balance typically appears in the next reporting cycle, usually within 30–45 days.

Does paying off credit cards always increase your score? It usually helps over time, but closing the account can temporarily raise utilization on remaining cards and affect other factors like Credit Mix & Account Types.

Is 0% utilization good? It is better than high utilization, but not optimal long-term. Low single-digit usage better demonstrates responsible, active credit management without appearing inactive.

How long until lower utilization improves my score? Expect visible changes within 30–45 days once all relevant issuers report the new, lower balances.

Can utilization change without new spending? Yes. Shifts often result from reporting timing differences, credit limit adjustments, or asynchronous updates across accounts.

Related Reading from the Complete Credit Scoring Education Framework:

This comprehensive guide equips you with the knowledge and tactics to treat utilization as a controllable advantage rather than a source of confusion. Apply these principles consistently across the full Complete Credit Scoring Education Framework, and you’ll build a more resilient, higher-scoring credit profile that serves your financial goals for years to come.