Follow the Credit System Step-by-Step

Why Is My Credit Score Different on Experian, Equifax, and TransUnion? (Why Credit Scores Don’t Match)

Why are your credit scores different on Experian, Equifax, and TransUnion—and why do they never seem to match across apps like Credit Karma or your bank? This guide breaks down one of the most common and confusing patterns in credit systems: why credit scores don’t match. Learn how different credit bureaus collect data, how scoring models like FICO and VantageScore interpret that data, and why timing alone can create different scores—even when your financial behavior stays the same. If you’ve ever wondered why you see a different credit score on each app, or why your Credit Karma score is different from your bank, this article explains the real system behind it in clear, simple terms.

CreditPatterns.com

4/21/20268 min read

This is one of the most common reasons people search why their credit scores don’t match across apps and credit bureaus.

You’re sitting at the kitchen table after dinner, phone in hand, just trying to get a clear picture of where things stand. Maybe a big purchase is on the horizon, or you’re simply curious after months of steady payments. You open one site and see a number that feels reassuring—solid, expected. A few minutes later, on another platform, the number shifts. Sometimes it’s higher. Sometimes noticeably lower. The same life. The same financial decisions. Yet the scores refuse to line up.

That quiet jolt of confusion hits hard. It can make you question whether something is wrong with your records, or whether the systems themselves are unreliable. But this pattern is often observed for deeply structural reasons, as explained in the Credit Scoring Framework and based on how credit data is reported.

Why Is My Credit Score Different on Experian, Equifax, and TransUnion?

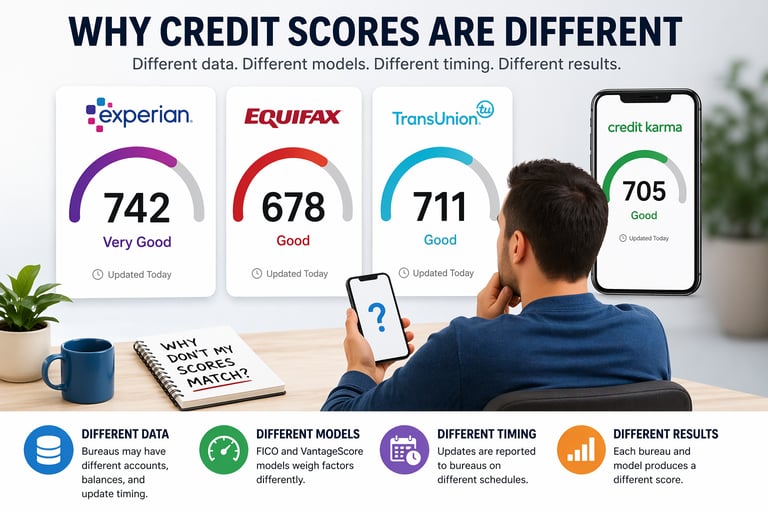

Credit scores are different across bureaus because each bureau may have different reported data, scoring models may interpret that data differently, and updates occur at different times, which is one of the main reasons credit scores don’t match across different apps and credit bureaus. As a result, each score reflects a slightly different version of the same credit profile.

Credit scores don’t match because there is no single system generating one number. Instead, multiple independent systems evaluate different versions of the same data at different times.

🧩 The System Perspective To understand why this happens, it helps to view it through the broader Credit Patterns framework. Credit scoring is not one unified system. It consists of multiple independent layers of data reporting, model interpretation, and profile evaluation happening in parallel across the major bureaus.

Why Experian, Equifax, and TransUnion Show Different Scores

Each credit bureau operates as an independent data system. Experian, Equifax, and TransUnion may receive different account updates, at different times, from different lenders. As a result, the data each bureau uses to generate a score may not be identical at any given moment.

From a scoring model perspective, these become distinct profiles—even though they represent the same individual. The system evaluates what has actually been reported to it, not an idealized complete picture.

What Is a Credit Bureau?

A credit bureau is a data reporting agency that collects and maintains credit information from lenders. Experian, Equifax, and TransUnion each build independent credit files based on the data they receive. This is why many people search for why their credit scores are different across bureaus or apps.

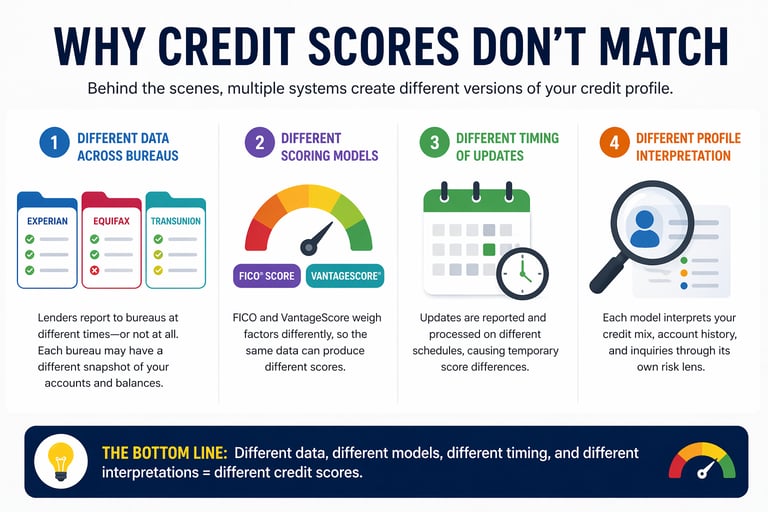

🧠 The First Layer: Different Data Across Bureaus As detailed in how credit data is reported, lenders and creditors are not required to report to every bureau equally or on the same schedule. One bureau might include a recent account opening or balance update, while another shows a more limited or outdated view.

📊 A Common Pattern Observed: The Incomplete or Lagging File Picture someone who recently paid down a balance or added a new line of credit. One bureau may have already received and incorporated that update, reflecting a fresher snapshot. Another bureau might still be working with data from weeks earlier. Scoring models then analyze these slightly divergent datasets, and the resulting profile reflects those differences.

Why Credit Scores Don’t Match Across Apps Like Credit Karma and Banks

This pattern is often observed because different platforms may use different scoring models and pull data from different credit bureaus. One app may display a VantageScore based on TransUnion data, while another may show a FICO score based on Experian data. From a system perspective, these are different datasets being interpreted by different models, which leads to different results. This is why many people notice their credit karma score is different from their bank or lender score. This is also why people notice a FICO vs VantageScore difference when comparing scores across platforms.

A Real-World Scenario That Explains This

A person checks their credit score on one platform and sees a recent balance update reflected. On another platform, the balance hasn’t been updated yet. From a scoring model perspective, these are two different data snapshots being evaluated separately. The system reflects those differences, even though the underlying behavior is the same.

In another case, one bureau may include a recently opened account while another does not yet reflect it. From a scoring model perspective, this changes the structure of the profile, leading to different score outputs. This helps explain why you might see a different credit score on each app.

🧠 The Second Layer: Different Scoring Models Even if the data were perfectly aligned, scores can still vary. This occurs because different scoring models weigh factors with varying emphasis, as explained in how scoring models work. The framework shows how models respond differently to patterns, such as those explored in the Credit Utilization & Credit Card Behavior Framework.

The system tends to interpret the same elements through slightly different risk perspectives, leading to different numerical outcomes.

🧠 The Third Layer: Timing of Updates Credit reporting does not happen in real time. Updates arrive at each bureau on independent cycles. A payment or balance change might appear on one bureau days—or weeks—before it shows on another. This creates temporary but meaningful differences in the data snapshots that scoring models evaluate.

🧠 The Fourth Layer: Holistic Profile Interpretation Subtle variations in account age, credit mix, or inquiry patterns can further influence how the full file is understood. These elements connect to the Credit Age & File Depth Framework, the Credit Mix & Account Types Framework, and the Credit Inquiries & New Credit Activity Framework.

Scoring models evaluate the interconnected story presented by the available data, not isolated pieces.

🔍 Observing These Patterns with SmartCredit and myScoreIQ (Affiliate Disclosure). Some users choose to observe these differences across bureaus and score variations across models using monitoring platforms. These tools allow visibility into how different systems interpret reported data over time, as outlined in the Credit Monitoring & Credit Tools Framework.

🧠 Final Perspective Shift The unease that comes with seeing mismatched scores isn’t usually a sign of a problem in your financial story. It is a reflection of something deeper: there is no single “credit score.” There are multiple evaluations occurring simultaneously, each shaped by its own data ecosystem, timing, and interpretive rules.

Why Credit Scores Don’t Match Is a System Pattern

This pattern is often observed across nearly all credit profiles. Because multiple bureaus, scoring models, and reporting timelines are involved, differences between scores are not unusual—they are expected outcomes of how the system operates.

If you’ve been trying to understand why your credit scores don’t match, this is one of the most consistent patterns observed across credit systems.

🎯 Key Takeaway The system does not ask, “What is your score?” It asks, “What does this particular dataset look like right now, under this specific model?” Recognizing this shifts the focus from chasing one definitive number to understanding the patterned behavior of multiple independent systems working side by side.

🔍 Observing These Patterns

Some users choose to observe how their credit scores differ across bureaus and models using monitoring tools.

Platforms like SmartCredit and myScoreIQ (Affiliate Disclosure) are commonly used to track how reported data changes over time and how scoring models respond to those updates. These tools provide visibility into credit data snapshots across different systems rather than influencing the scores themselves.

Related Questions People Ask

Why are my credit scores different on Credit Karma and Experian?

Why is my FICO score lower than my bank score?

Why do credit scores not match across apps?

Which credit score do lenders actually use?

Why is my mortgage score different from my credit card score?

Why does my credit score change daily?

How much difference between credit scores is normal?

❓ FAQs — Why Credit Scores Differ Across Bureaus

Why are my credit scores different on different apps? This pattern is often observed because different apps may pull data from different credit bureaus and apply different scoring models. Based on reported data, each platform may evaluate a slightly different version of the credit profile, leading to different results.

Why is my credit score different on my bank app vs Credit Karma? This pattern is often observed because different platforms may use different scoring models and pull data from different bureaus. Based on reported data, each system may evaluate a slightly different version of the credit profile.

Why is my credit score different on Experian, Equifax, and TransUnion? This pattern is often observed because each bureau may contain slightly different reported data. Not all lenders report to all three bureaus equally, and updates occur on independent schedules. As a result, scoring models evaluate different datasets and can produce different scores.

Why are my credit scores different on Credit Karma and Experian? This pattern is often observed because Credit Karma and similar platforms may use different scoring models or pull from specific bureaus at different times. The system evaluates the available data snapshot, which can vary across platforms.

Why is my FICO score different from my VantageScore? Scoring models may interpret the same data differently. FICO and VantageScore use distinct formulas and weighting, so the system tends to produce varying results even from similar reported data.

Which credit bureau is used the most? The system does not designate one bureau as primary. Lenders choose based on their own practices, and many pull data from multiple bureaus depending on the type of credit decision.

Why is my mortgage credit score different from my app score? Mortgage lenders often use specific FICO model versions tailored to mortgage risk. Consumer apps may apply different models or data snapshots, leading scoring models to evaluate the profile differently.

How far apart should my credit scores be? Differences between scores are commonly observed and can range from a few points to over 100 depending on data variation and models used. The profile simply reflects the reported data available to each system.

Do all three credit bureaus show the same credit score? No. Credit bureaus operate independently. The system does not require uniform reporting across all bureaus, so each one may reflect a slightly different version of the credit profile based on the data it has received.

Which credit score is the most accurate? There is no single “most accurate” score. Scoring models evaluate data differently depending on the specific model used and the dataset available at that moment. Each score reflects how a particular system interprets the reported information.

Why does my score change depending on where I check it? This pattern is often observed because different platforms may pull data from different bureaus or apply different scoring models. Timing of updates can also vary, leading scoring models to interpret slightly different snapshots.

Do lenders see the same credit score that I see online? Not always. Lenders may use proprietary scoring models or different versions than consumer-facing tools. The system evaluates the data differently depending on the model applied by the lender.

Why does one bureau show an account that another bureau does not? This occurs when a creditor reports information to one bureau but not to the others. Based on reported data, each bureau builds its own independent credit file, which can result in differences in what appears.

Can the timing of updates cause credit score differences across bureaus? Yes. Credit data is updated at different times across the bureaus. One bureau may reflect more recent information while another still shows an older snapshot, causing scoring models to produce varying results.

Do different scoring models use the exact same formula? No. Scoring models vary in how they weigh different factors. The system tends to interpret patterns differently depending on the model, which can lead to different score outputs from similar data.

Why do my scores sometimes appear closer together over time? This pattern is often observed when data updates across bureaus become more aligned. As reporting synchronizes, the differences between the datasets may narrow, causing scores to converge temporarily.

Is it normal for credit scores to be different across bureaus? Yes. This is a common and expected behavior in credit systems. Multiple bureaus, independent reporting, different scoring models, and varying update timing all contribute to these variations.

⚠️ Disclaimer Educational content only. Not credit repair advice or services. No guarantees made.