Follow the Credit System Step-by-Step

How Credit Age and File Depth Affect Your Credit Score (And Why It Matters More Than Most People Realize)

Discover how credit age and file depth affect your credit score in 2026. Learn why length of credit history matters, how average age of accounts impacts FICO and VantageScore, and proven ways to build long-term credit strength.

CreditPatterns.com

3/28/20265 min read

You’ve been doing everything right — paying every bill on time, keeping balances low, and avoiding new debt. Yet your credit score barely moves, or it feels strangely stuck no matter how responsible you are.

This frustration is incredibly common, and one of the biggest hidden reasons is credit age and file depth — how long you’ve had credit and how substantial your credit file has become over time.

Unlike payment history or utilization, credit age is one of the slowest factors to improve. It rewards patience and consistency. This makes it one of the most stable — but least immediately controllable — factors in modern credit scoring systems.

This guide is Step 6 in the Complete Credit Scoring Education Framework.

🔍 What Percentage of Your Credit Score Is Credit Age? Credit age typically accounts for about 15% of a FICO score and approximately 20–21% of a VantageScore, making it an important long-term factor in credit scoring models.

🔍 What Is Credit Age and File Depth? Credit age refers to the length of your credit history. Scoring models evaluate three main components: the age of your oldest account, the age of your newest account, and the average age of all your accounts. File depth measures how substantial your credit history is — the number of accounts, variety of account types, and overall thickness of your file over time.

Real-World Example Imagine two people with identical perfect payment records and low utilization. One has maintained accounts for 15 years. The other is just starting out with two years of history. The first person will usually see a meaningfully higher contribution from credit age and file depth, even though their recent behavior looks exactly the same.

Why Credit Age Matters in 2026 Scoring Models

In FICO models, length of credit history accounts for 15% of your score. In VantageScore 4.0, depth of credit (which heavily includes age and mix) weighs approximately 20–21%.

Scoring models value credit age because it reveals a longer track record of how someone handles credit through changing life circumstances and economic conditions — as explained within the Credit Scoring Models Framework.

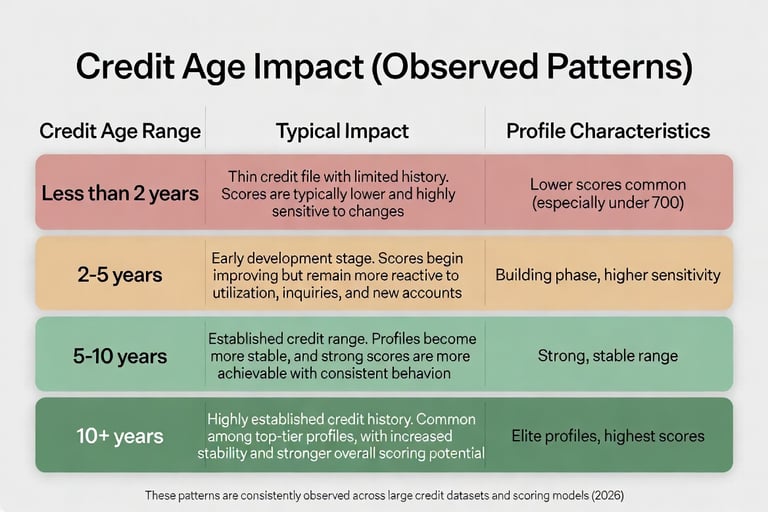

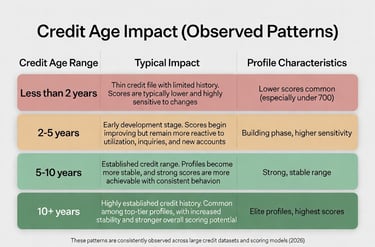

Credit Age Impact (Observed Patterns) Credit age tends to follow consistent patterns across most credit profiles:

Less than 2 years Thin credit file with limited history. Scores are typically lower and highly sensitive to changes.

2–5 years Early development stage. Scores begin improving but remain more reactive to utilization, inquiries, and new accounts.

5–10 years Established credit range. Profiles become more stable, and strong scores become more achievable with consistent behavior.

10+ years Highly established credit history. Common among top-tier profiles, with increased stability and stronger overall scoring potential.

These patterns are not fixed rules, but they are consistently observed across large credit datasets and scoring models.

🔍 What Is Average Age of Accounts? Average age of accounts is calculated by adding the age of all credit accounts and dividing by the total number of accounts, representing the overall maturity of your credit profile.

Why Credit Age Feels Slow Your Action → Pay on time and keep balances low System Effect → Minimal immediate change Long-Term Result → Gradual score improvement

Credit age builds silently over time, not instantly through behavior.

🔍 Does Opening a New Account Hurt Credit Age? Yes. Opening a new account lowers your average age of accounts and can temporarily reduce the positive impact of your existing credit history.

How Credit Age Interacts With Other Factors

Credit age rarely works alone. It strongly amplifies or offsets other major factors as part of score movement patterns in the Credit Score Changes & Fluctuations Framework and as explained in the Credit Data Reporting & Structure Framework:

Perfect payments on older accounts carry significantly more weight.

Long-standing accounts with low utilization create an especially positive impression.

A diverse mix maintained over many years strengthens overall file depth.

Proven Strategies to Build Credit Age and File Depth Responsibly in 2026

Keep Old Accounts Open The single most powerful action is to avoid closing old credit cards or loans that are in good standing. These accounts continue to age and positively influence your average age and file depth.

Become an Authorized User Strategically Being added as an authorized user on a long-standing, responsibly managed family account can sometimes add positive age and depth to your file (results vary depending on the bureau and scoring model).

Avoid Opening Too Many New Accounts Quickly New accounts temporarily lower your average age and can reduce the positive impact of your existing file depth.

Monitor Your Credit Age Over Time Regularly tracking how your average account age and file depth change across reporting cycles provides valuable insight into your credit profile’s development.

Pro Tip: If you’re planning a major purchase such as a mortgage or auto loan, lenders will pay close attention to your credit age. Starting to build it early creates a meaningful long-term advantage.

Observing how credit age develops over time can provide additional context beyond a single snapshot of your credit score. Some individuals choose to periodically review their credit profile to observe how account age and file depth evolve over time. Because credit age is based on reported account history rather than real-time changes, reviewing your profile can help connect how older accounts, new accounts, and average age are being reflected within the system. 👉 View your credit profile here Affiliate Disclosure

This allows for observation of how your credit file develops over time, but results may vary based on scoring model, credit bureau, and timing of updates.

The Bigger Picture: Credit Age in the Full Credit System

To truly understand your score, zoom out and view credit age and file depth as one important piece of the Complete Credit Scoring Education Framework. It connects directly to how data is reported, how scoring models interpret long-term patterns, and how credit scores evolve over many months and years.

In practice, individuals who maintain older accounts responsibly while managing utilization and payments well often experience compounding positive effects as their credit age naturally matures.

Key Takeaways

Credit age and file depth demonstrate your long-term track record of credit management to lenders.

This factor accounts for 15% of FICO scores and approximately 20–21% of VantageScore — it changes slowly but becomes highly influential for excellent scores.

The most effective strategy is patience and preservation: keep old accounts open and in good standing.

While newer models offer slightly more flexibility for thinner files, a strong, seasoned credit history remains one of the most stable foundations for a high credit score.

Mastering credit age won’t deliver fast results, but it builds one of the most reliable pillars for long-term credit strength.

Observing how credit age fits into the larger credit system reveals patterns that are not visible when focusing on a single snapshot. When you begin to track how your file depth evolves over time — not just your most recent activity — you shift from simply reacting to score changes to intentionally building lasting credit strength with precision.

FAQ: Credit Age and File Depth Questions Answered

What is considered a good credit age? An average account age of 7+ years is generally solid, while 10+ years is excellent and commonly seen in top-tier 800+ FICO profiles.

Does closing an old credit card hurt your credit age? Yes. Closing old accounts can lower your average age and reduce file depth, particularly if the card had a long positive history.

How long does it take for credit age to improve a credit score? Credit age improves gradually over months and years as accounts continue to age. There is no quick fix for this factor.

Can you build credit age quickly? Not significantly. Becoming an authorized user on seasoned accounts can provide some benefit, but time remains the primary driver.

Does credit age matter more than credit utilization? No. Payment history (35%) and utilization (30%) still carry greater weight individually, but credit age becomes increasingly important as you pursue very high scores.

Related Reading from the Complete Credit Scoring Education Framework:

Previous Step: Credit Utilization & Credit Card Behavior Next Step: Credit Mix & Account Types Framework