Follow the Credit System Step-by-Step

How Long Hard Inquiries Really Affect Your Credit Score (The Timing Pattern Most Advice Gets Wrong)

Worried a credit application will damage your score for years? Hard inquiries have far less impact and shorter duration than most advice suggests. Discover the precise timing mechanics, original patterns, and practical steps to protect your score during rate shopping or major life moves.

CreditPatterns.com

3/31/20267 min read

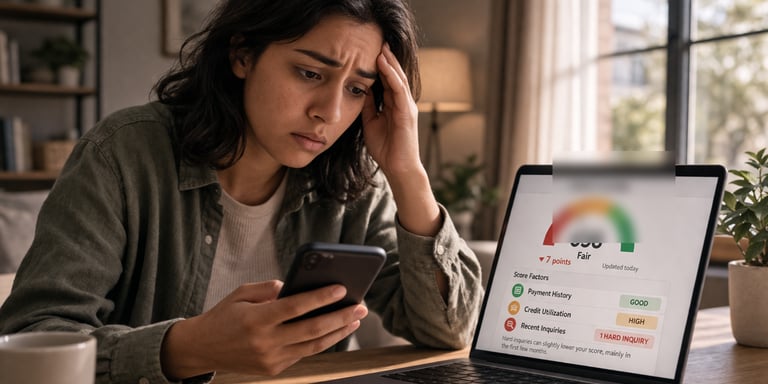

You hit submit on a credit application and watch your score drop a few points. Then another pull comes through, and the quiet worry sets in: How long will this keep affecting me? Will it raise my rates or quietly block approvals when it matters most?

A single credit application can cost you points — but not for the reason most people think.

Hard inquiries remain visible on your credit report for up to two years, but their actual influence on your score is far more limited than most people fear. The strongest impact usually occurs in the first 1–3 months and fades significantly, becoming largely irrelevant to most scoring calculations after about 12 months. This gap between long visibility and short scoring weight creates far more anxiety than the actual damage typically causes.

This is how credit scoring works as a system—not isolated factors, but patterns interacting over time.

Unlike most articles that simply state “2 years on the report, 1 year on the score” and stop there, this piece explores the precise timing mechanics, original patterns, and system-level interactions that actually determine how much — and for how long — hard inquiries affect you.

A single hard inquiry typically causes a small temporary drop — often fewer than 5 points on FICO scores and 5–10 points on VantageScore — with the peak negative effect concentrated in the first 1–3 months. The severity depends heavily on your broader credit profile. With long credit history and low utilization, one inquiry may produce almost no visible drop. Multiple unrelated inquiries clustered in a short window, however, can create a moderate combined impact of 10–20+ points because they intensify the perceived risk signal.

Here’s where it gets confusing: the inquiry you see lingering on your report is not quietly eroding your score month after month.

The underlying system cause is risk signaling. Scoring models interpret recent applications for new credit as a potential sign of increased borrowing needs or financial pressure. The visible trigger is the hard pull itself — when a lender formally requests your full credit file with your permission.

This ties directly into how new credit affects your score, where we see how inquiries interact with other factors in real time. It also connects to the broader Credit Patterns Framework, which explains how all pieces of your credit file influence each other.

Score impact registers within days of the inquiry being reported to the bureaus because models update using the freshest data available. The strongest negative weight occurs in the first 1–3 months, then gradually fades. Most models stop factoring the inquiry after approximately 12 months. Recovery accelerates when time passes alongside consistent positive behaviors such as on-time payments and stable or improving utilization.

This is what most people miss: hard inquiries make up only about 10% of a FICO score, yet their timing can noticeably amplify or mute the effects of other major factors like utilization and credit age.

At their core, hard inquiries operate through a set of interconnected patterns that together form one unified mental model of how the credit system evaluates recent credit-seeking behavior.

Recency Amplification Effect makes the negative influence heaviest immediately after an inquiry posts. Models prioritize very recent behavior as the strongest predictor of near-term risk, so the first 30–90 days carry the most weight. This pattern affects short-term approvals and rates most strongly and interacts powerfully with high utilization or recent new accounts.

Rate-Shopping Grace Window treats multiple inquiries for the same loan type within 14–45 days as one. Models recognize legitimate rate comparison rather than desperation, protecting the new credit factor and preventing unnecessary cumulative damage during major purchases.

Inquiry Horizon Disconnect (original pattern) is the most important and least discussed dynamic: a clear horizon separates long report visibility (up to 24 months) from short scoring relevance (roughly 12 months). Reports provide full historical transparency to lenders, while scoring algorithms deliberately use only recent, predictive data. After the 12-month mark, the inquiry no longer affects automated scores but can still influence manual underwriting reviews.

Clustering Cascade occurs when unrelated hard inquiries in quick succession create a compounded risk signal. Multiple pulls suggest possible financial strain, so the combined effect exceeds simple addition. This pattern works against recovery from strong payment history or utilization improvements and is most dangerous during tight financial periods.

Offset Acceleration Pattern shows that consistent positive behaviors can neutralize inquiry effects faster than time alone. Because models evaluate the entire profile holistically, strong on-time payments and low utilization create counter-pressure that accelerates recovery. This pattern explains why two people with the same number of inquiries can experience very different outcomes.

Here’s how all these patterns work together: The system doesn’t punish the act of applying for credit. It reacts to the recency, clustering, and context of those applications relative to everything else in your file. Recency amplifies risk, clustering compounds it, the horizon disconnect creates lingering confusion, and offset behaviors provide the fastest way out. Together they form one cohesive mental model: hard inquiries are a short-term timing signal, not a long-term penalty.

Maria in Phoenix, Arizona was deep into mortgage pre-approval when she opened a new balance-transfer card to consolidate debt. Her score dropped 7 points right as the lender ran another pull. The stress was immediate — she could already picture higher interest rates making the monthly payment stretch her family’s budget too thin, potentially forcing them to delay their dream home or settle for a smaller house. Understanding the Recency Amplification Effect and Inquiry Horizon Disconnect allowed her to pause further applications and lean on her strong payment record. Within 90 days the impact had largely faded, and she closed on the house with better terms than she had feared.

Tyler in Cleveland, Ohio applied for an auto loan, a personal loan, and a store card within a three-week window during a cash-flow crunch. His score fell a combined 19 points just before finalizing the car purchase. The uncertainty kept him up at night — every “what if” about denial or worse rates made the entire deal feel precarious. Learning the Clustering Cascade and Offset Acceleration Pattern helped him stop unnecessary pulls and focus on his low utilization. Four months later the score had recovered sufficiently, restoring his confidence and securing favorable financing.

At this point, many people realize they don’t actually have visibility into how inquiries and other factors are shifting month to month. This is where real-time monitoring tools can quietly make a difference. Affiliate Disclosure

Common misunderstandings often make the situation feel worse than it is. Many believe a hard inquiry will ruin their score for years, but the scoring impact is small and typically irrelevant after 12 months. Others assume all inquiries hurt equally, ignoring how rate-shopping windows and overall profile strength create massive differences. Some expect the score to improve the moment the inquiry falls off the report, when recovery usually happens well before the two-year visibility period ends. And many think one inquiry is harmless with otherwise excellent credit, yet clustering can still produce noticeable moderate effects.

Replacing these assumptions with accurate pattern understanding eliminates unnecessary fear and supports better decisions.

Strategic takeaways flow naturally from this understanding. Space out unrelated credit applications when possible, take full advantage of rate-shopping grace windows for the same loan type, and maintain strong payment history with controlled utilization to accelerate recovery. Review your credit reports periodically to distinguish authorized pulls and catch errors early. These actions work because they respect how the system actually processes timing and context — not because they are clever tricks.

To minimize hard inquiry impact before a major application, group rate shopping within the 14–45 day window and prioritize responsible habits. Positive behaviors like on-time payments and low utilization help the score recover faster than simply waiting for time to pass.

FAQ

Why do hard inquiries affect my credit score? Hard inquiries signal recent credit-seeking behavior, which models interpret as potential increased risk. They typically account for about 10% of FICO scores, with a single inquiry causing only a small temporary drop for most people.

How long do hard inquiries stay on your credit report? Hard inquiries remain visible on your credit reports for up to two years. However, their influence on most scoring calculations ends after approximately 12 months.

How much does one hard inquiry lower a credit score? A single hard inquiry usually drops a FICO score by fewer than 5 points and a VantageScore by 5–10 points. The exact impact depends heavily on your overall profile depth and other recent activity.

What is the difference between hard and soft inquiries? Hard inquiries occur when you formally apply for credit and can temporarily affect scores. Soft inquiries (pre-approvals or your own monitoring) never impact your credit score.

Do multiple hard inquiries hurt more than one? Yes, especially when they are for different credit types and occur close together. Rate-shopping for the same loan type within the grace window is usually counted as one inquiry.

How long until a hard inquiry stops affecting my score? The strongest effect occurs in the first 1–3 months and fades gradually. Most models no longer factor it after about 12 months.

Can I remove a hard inquiry from my credit report? Only if it is inaccurate or unauthorized. Legitimate hard inquiries you authorized cannot be removed early.

Does a hard inquiry affect mortgage or auto loan approvals? It can have a minor effect if recent or clustered, but strong payment history and low utilization often outweigh the temporary dip. Lenders also review inquiries manually.

Why do different scoring models treat inquiries differently? FICO generally looks back only 12 months, while some VantageScore versions may consider up to 24 months. Grace windows for rate shopping also vary slightly by model.

What happens if I have several hard inquiries in a short time? Multiple unrelated inquiries can create a moderate combined impact. Rate-shopping for the same loan type within the grace window usually counts as one.

How can I avoid hard inquiry surprises before a big financial decision? Many people use real-time credit monitoring tools that alert them to new inquiries and show how they interact with the rest of their profile, providing early visibility for better decisions.

Conclusion

Hard inquiries highlight how scoring models weigh recent credit-seeking signals against your longer-term patterns. When you understand the short scoring horizon versus longer report visibility — and how positive behaviors can accelerate recovery — you move from reactive anxiety to deliberate control.

Your credit score responds to the recency, clustering, and context of inquiries within the full system — not merely to their presence on the report.

This deeper understanding connects directly to how new credit affects your score, credit utilization patterns, and why your credit score changes. The clearer these interconnections become, the more confidently you can navigate credit decisions.t content