Follow the Credit System Step-by-Step

How a Credit Limit Increase Changes Your Credit Score (Without Spending More)

In this article, we break down how a credit limit increase can change your credit score without any new purchases or payments. You’ll learn how scoring models reinterpret your profile through shifting ratios, capacity, and structural relationships — and why even a single change can affect multiple variables at once.

CreditPatterns.com

4/11/20264 min read

A credit limit increase appears simple — more available credit, no change in spending, no change in habits. Many expect the scoring system to register this neutrally or favorably.

Yet the models respond with a more precise structural adjustment. The increase does not simply add room to borrow. It forces a recalculation of how every existing balance and account relates to the updated capacity, reshaping the context in which the entire credit profile is measured.

The Pattern This movement follows a structural pattern driven by ratios rather than any change in payment behavior. Scoring algorithms continuously compare revolving balances against available credit. When the limit on one account expands, the underlying relationships across the file shift automatically — even if every dollar owed and every payment stays identical. The new reading only becomes visible once the updated data completes its journey through reporting cycles.

What the System Is Measuring Credit scoring models evaluate interconnected relationships across the full file, not isolated figures. They track how total revolving balances sit against total available credit and how individual account limits influence the overall distribution of capacity.

These calculations form a core part of how revolving balances are interpreted inside the credit utilization and credit card behavior framework, where the system evaluates not just raw usage percentages but how efficiently available credit is being managed across multiple accounts. A limit increase alters the denominator in those calculations, prompting the models to re-weight that account’s contribution within the broader credit data reporting and structure framework.

Why This Can Affect a Score The effect arises from layered mechanical recalibrations inside the algorithms. These adjustments do not occur in isolation. When the system recalculates utilization on the affected account, it simultaneously rebalances how that account contributes to aggregate metrics across the entire file. This means a single limit increase can subtly influence multiple scoring variables at once, even though only one input changed.

In many scoring models, this recalculation occurs simultaneously at both the individual account level and the aggregated profile level, meaning the same change is interpreted through multiple scoring lenses at once.

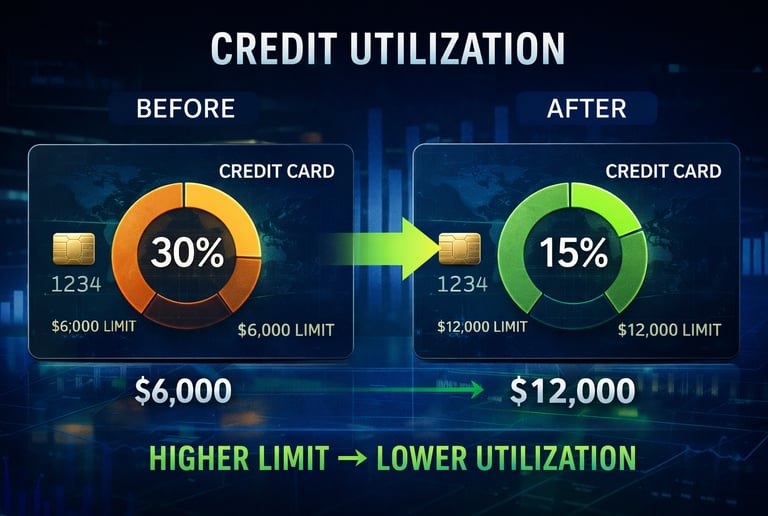

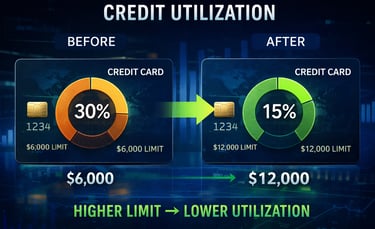

Utilization Compression A card carrying a $1,800 balance on a $6,000 limit reflects 30% utilization. If the limit rises to $12,000 while the balance remains unchanged, the same $1,800 now equals 15%. The models register this lower relative usage, which can shift the revolving component without any new charges or payments.

Profile Rebalancing Because accounts interact within the full structure, the expanded limit changes the relative weight of that revolving line. This rebalancing causes neighboring accounts to be interpreted through a slightly adjusted lens.

Risk Signal Adjustment Greater demonstrated capacity paired with stable balances leads the models to reinterpret overall exposure levels. Within the credit scoring models framework, these interactions can produce movement that reflects the new structural context rather than any behavioral shift.

Timing & Reporting The impact rarely appears immediately. Lenders report updated limits according to their billing cycles, credit bureaus incorporate the data during refreshes, and scoring models then re-evaluate the file. This sequence connects directly to the patterns explained in the hidden patterns behind unexpected score changes, where even positive structural shifts can coincide with temporary fluctuations due to reporting timing.

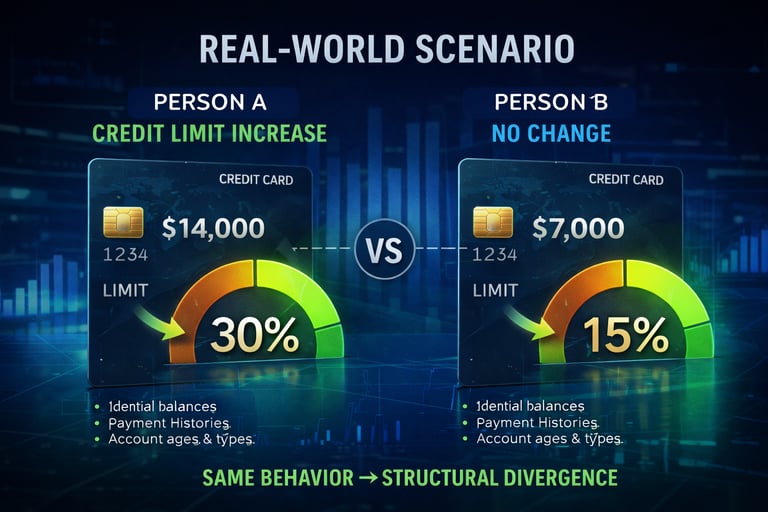

Real-World Scenario Two credit files begin with identical balances, payment histories, account ages, and types. Person A receives a limit increase on one card from $7,000 to $14,000. Person B sees no change.

Once the lender reports the new limit and the bureaus process the update, the files diverge structurally. The models now measure the same balances against different capacity levels, causing one profile to reflect movement while the other stays steady — all without any difference in spending or payment behavior.

Common Misinterpretations

“A limit increase will always raise the score.” The actual direction depends on how the new ratios interact with the rest of the profile — not every expansion compresses utilization in a way that produces the expected lift.

“No new spending means nothing changed.” The system does not evaluate behavior in isolation — it evaluates relationships. When those relationships shift, movement can occur without any new activity.

“Higher limits are universally positive.” The rebalancing effect can sometimes highlight or offset other file elements in ways that temper the outcome.

The Bigger Pattern Credit scoring models weigh context as heavily as conduct. A credit limit increase introduces no new behavior, yet it changes the lens through which existing behavior is assessed. This sensitivity to file structure at any snapshot in time echoes dynamics seen in the credit mix and account types framework, where the composition and capacity of accounts continuously shape interpretation.

The system does not need new behavior to produce a new outcome. It only needs a different way to measure the behavior that already exists.

FAQ

Why might a credit score change after a limit increase even with no spending? The models recalculate utilization and capacity ratios using the updated limits, which alters how the revolving portion of the profile is read overall.

How long until a limit increase typically affects the score? It usually appears after the lender reports the change and bureaus complete their update, often aligning with monthly cycles and subsequent model refreshes.

Can a limit increase ever align with a score drop? Yes, particularly when the structural shift interacts with other file elements differently or when reporting timing creates a temporary mismatch.

Do different scoring models respond the same to limit increases? No. Variations in how models weigh utilization, capacity distribution, and account interactions can lead to different short-term readings.

Does a change on one account affect the whole credit profile? Even a single revolving adjustment can influence aggregated metrics and profile weighting, since the system evaluates relationships across all reported data.

Closing Thought A credit limit increase leaves habits untouched but modifies the structural context in which those habits are measured. In a system driven by ratios and periodic re-evaluation, that contextual shift alone can be enough to produce observable movement.

Disclaimer This content is for educational purposes only and does not constitute financial advice or credit repair services. CreditPatterns.com explains how credit systems work — not how to manipulate them.