Follow the Credit System Step-by-Step

Why Did My Credit Score Drop Suddenly? The Hidden Patterns Behind Unexpected Changes

Why did your credit score drop suddenly—even when nothing changed? Learn the real system patterns behind score fluctuations, including utilization, reporting timing, and multi-factor interactions most people never see

CrediPatterns.com

4/3/20266 min read

A sudden credit score drop is most commonly linked to reporting timing, utilization changes, or multi-factor interactions within the scoring system.

Many people search for answers when they notice their credit score dropped suddenly, often wondering why it happened even when nothing obvious changed in their financial habits. In many cases, this pattern stems from how credit scoring models evaluate snapshots of reported data rather than ongoing behavior. Lenders report account information on their own cycles, so a temporary shift in a balance or timing mismatch can cause the score to adjust, even if payments were made on time.

This behavior is a core part of the credit scoring system and is explained in detail within the Credit Scoring Education Framework. This pattern is consistently observed across the broader credit scoring system and is explained in detail within the Credit Scoring Education Framework. The confusion often hits hardest when the drop appears random. One day the number looks stable, the next it moves noticeably. This pattern is frequently observed because scoring systems recalculate risk based on the most recent data fed into the bureaus, not real-time actions.

At that point, many people start looking for a way to see what actually changed behind the scenes rather than guessing, which is where tools like SmartCredit (Affiliate Disclosure) are sometimes used to visualize reporting timing more clearly.

The Moment the Drop Feels Personal

It usually begins with a routine check. Everything seemed steady—no missed payments, no new accounts, consistent habits. Then the score appears lower than expected. That sudden change creates a wave of uncertainty, as if the system shifted without warning.

This feeling is common because most individuals focus on their own actions while the scoring models focus on whatever data was reported at a specific moment. The gap between personal effort and reported information often leads to these unexpected movements.

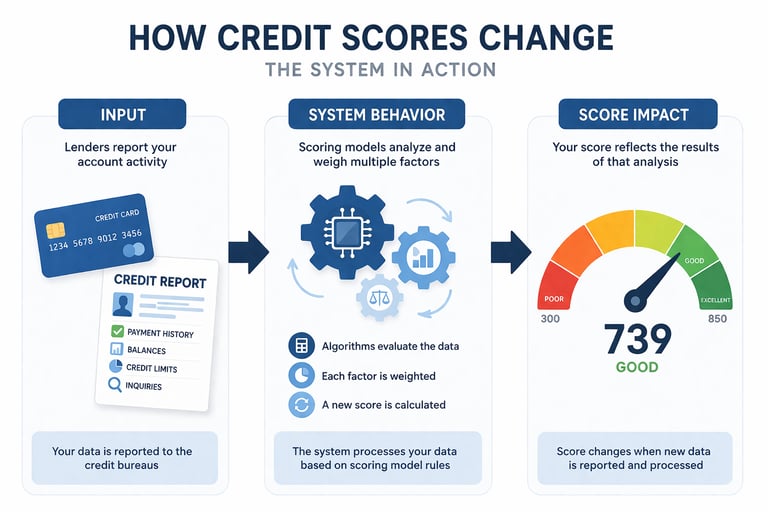

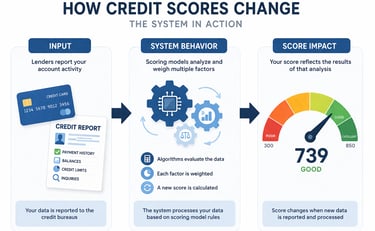

System Breakdown: Input → Behavior → Impact

Credit scoring models operate on inputs from lenders: balances, payment status, account ages, and inquiries. The system processes these at different times depending on each creditor’s reporting schedule.

When a new snapshot arrives—such as a balance captured before a payment fully posts—the model recalculates the overall risk profile. Even small changes in credit utilization or account status can produce a visible score adjustment. This input-to-impact flow explains why fluctuations occur even in stable profiles and shows how credit scores change over time. These patterns are also part of broader credit score fluctuation patterns explained across different reporting cycles.

Deep Patterns Behind the Changes

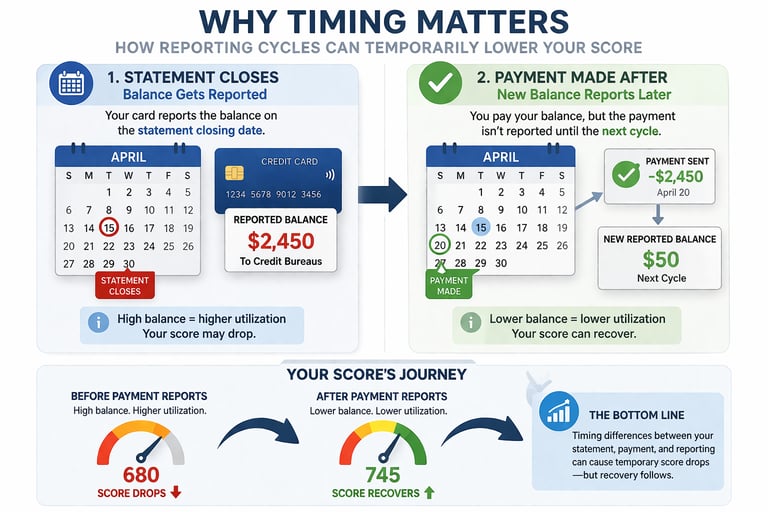

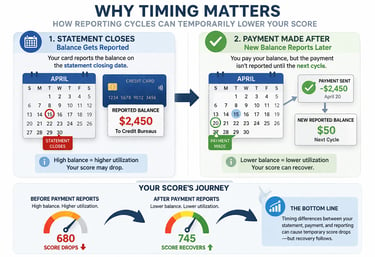

Timing plays a central role in these movements. Statement closing dates and reporting cycles do not always align with payment dates. In many cases, a card balance reports higher for one cycle before the payment reflects, temporarily raising utilization and prompting the model to adjust the score downward. This is a key element of how reporting timing affects your credit score. This same timing behavior is also connected to the Credit Data Reporting & Structure Framework.

Utilization patterns show up frequently as well. The system tends to respond to the proportion of available credit being used across revolving accounts. A slight increase in reported balances—sometimes from normal spending—can shift this ratio enough to affect the score until the next update. These dynamics are explored in detail through how credit utilization actually works. These same utilization patterns are also closely tied to how credit scores change over time, especially across reporting cycles.

Reporting cycles add another layer. Creditors do not all report on the same day, so updates can arrive staggered across the month. This creates natural variability as different pieces of data enter the profile at different times.

Multi-factor interactions amplify the effect. When a higher balance coincides with another update, such as an account status change or a new inquiry appearing, the combined impact on the scoring models can produce a larger shift than any single element alone. This reflects how scoring models interpret multiple variables.

When this starts happening, the biggest shift usually comes from simply seeing what the system is actually capturing instead of guessing. Some individuals use SmartCredit (Affiliate Disclosure) to track when balances are reported versus when payments are made, because that timing gap is often where these sudden score changes begin to make sense.

Real-World Scenarios Where This Pattern Appears

One commonly observed situation involves everyday credit card use. An individual charges normal expenses and pays the balance in full, yet the statement closes first. The reported balance appears higher for that cycle, and the score adjusts accordingly. This pattern often connects to how credit utilization affects your credit score and why it changes even when you pay on time.

Another scenario occurs after paying off an installment loan. The system may interpret the closed or paid account as a reduction in credit mix or history length, leading to a temporary drop even though overall debt decreased.

In “nothing changed” situations, the drop frequently traces back to subtle reporting differences across bureaus or a credit limit adjustment by a lender. This aligns with patterns seen in why your credit score dropped for no reason: hidden patterns explained.

Monthly fluctuations are especially common due to the staggered nature of updates—some accounts report mid-month while others update at the end.

Why It Feels Random (But Follows Clear Patterns)

The sense of randomness comes from the lack of immediate visibility into reporting timing. From an individual’s viewpoint, habits remained consistent, yet the number moved. In reality, the scoring models are doing exactly what they are designed to do: evaluating the latest available data snapshot and adjusting the risk assessment.

This is not arbitrary behavior. It reflects consistent system mechanics around data input, processing cycles, and variable interactions. Once the timing and snapshot nature become clearer, these movements stop feeling mysterious and start appearing as predictable credit score fluctuation patterns explained. These behaviors are also directly connected to how credit scores change over time within the broader system.

When multiple variables update at once, it becomes difficult to isolate what actually changed. Some individuals use SmartCredit (Affiliate Disclosure) to compare bureau updates side-by-side, which often makes these overlapping patterns much easier to recognize.

The deeper mechanics are explored further in the Credit Scoring Education Framework and the Credit Scoring Models Framework, where variable interactions are broken down in detail.

Over longer periods, these patterns tend to repeat in cycles rather than one-time events. Some individuals use mySCOREIQ (Affiliate Disclosure) to observe how their credit profile evolves across multiple reporting periods, which can make these fluctuations far more predictable over time.

Confusion Resolution: Seeing the System Clearly

What feels like a penalty is usually the model responding to a temporary data state. The system is not reacting to intent or long-term reliability in that moment—it is calculating based on the information present right then.

Understanding the Credit Data Reporting & Structure Framework helps clarify that these shifts follow structured rules rather than chance. The Credit Utilization & Credit Card Behavior patterns explain why timing gaps matter more than many realize.

At that point, the focus usually shifts from reacting to individual score changes to understanding the pattern behind them. Some individuals continue using tools like SmartCredit (Affiliate Disclosure) or mySCOREIQ (Affiliate Disclosure) to monitor how these patterns repeat over time, rather than focusing on single fluctuations.

The Pattern Most People Miss

One of the most overlooked aspects of credit scoring is that these changes are rarely isolated events. Instead, they tend to repeat based on reporting cycles, balance timing, and model recalculations. Once this pattern is recognized, what initially feels unpredictable begins to follow a consistent rhythm.

FAQs

Why did my credit score drop even though I paid everything on time?

In many cases, the system captured the balance before the payment was fully reflected in the report, creating a temporary increase in utilization that the scoring models responded to.

Why does my credit score change every month?

Reporting cycles vary by lender, so new snapshots of balances and account status arrive at different times. This staggered input commonly leads to monthly fluctuations as the models recalculate.

Why did my credit score drop suddenly with no obvious changes?

The drop is often tied to a reporting timing mismatch or multi-factor interaction that was not immediately visible, such as a balance snapshot or bureau update difference.

Can paying off debt cause a credit score to drop?

Yes, this pattern is frequently observed when an installment account closes or the credit mix shifts, even though overall debt decreased.

Will the score go back up after a sudden drop?

In cases driven by timing or temporary utilization changes, the score often adjusts again once the next clean reporting cycle arrives.

Why do different bureaus show different scores at the same time?

Each bureau receives updates on its own schedule, so the data snapshots can differ slightly, leading the scoring models to produce varying results.

Is a big drop always permanent?

Larger movements are commonly linked to multiple factors interacting at once, but many resolve or moderate as updated data flows in over subsequent cycles.

Final Summary

Recognizing these mechanics through the Credit Scoring Education Framework, Credit Data Reporting & Structure Framework, Credit Utilization & Credit Card Behavior, and Credit Score Changes & Fluctuations Framework helps connect what initially feels like separate events into one consistent system. When viewed together, these patterns explain why sudden drops, monthly fluctuations, and unexpected changes all follow the same underlying structure.

These patterns are not isolated events but repeating system behaviors, which is why the same types of score changes tend to appear across different profiles over time.

Affiliate Transparency

Some links mentioned may be affiliate partnerships. These tools are referenced for educational visibility into how credit reporting patterns behave.

Disclaimer

Educational content only. Not credit repair, financial, or legal advice. No guarantees are made.