Follow the Credit System Step-by-Step

Why Did My Credit Score Go Down After I Paid Off My Credit Card? (The Real Pattern Explained)

Why your credit score can drop after paying off a credit card—and the pattern behind it.

CreditPatterns.com

4/8/20265 min read

Sarah sat at her kitchen table in Lee’s Summit, staring at her phone with a sinking feeling in her chest.

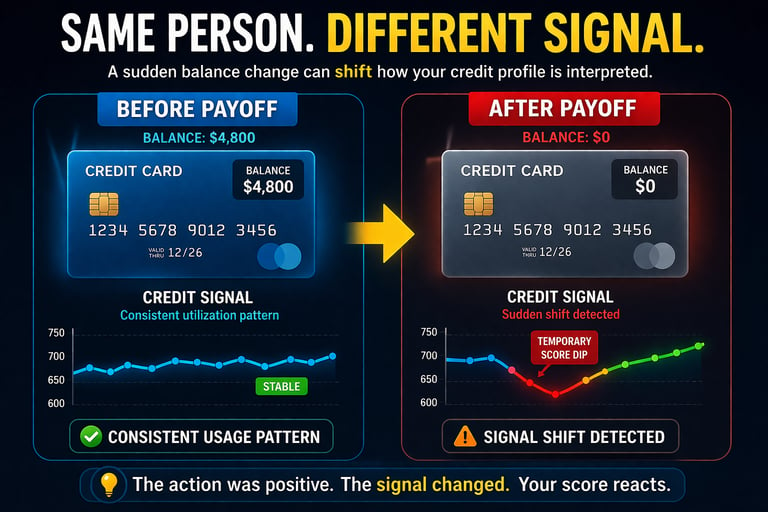

She had just done everything right. After months of careful budgeting and saying no to little extras, she finally paid off her credit card in full. The balance went from $4,800 down to zero. She felt a quiet sense of pride wash over her — like she was finally getting control of her money. She even poured herself a fresh cup of coffee, thinking this was a small but meaningful win.

Then the notification hit.

Her credit score had dropped. Not by five or ten points — by 28 points.

The frustration and confusion hit her all at once. “I did the responsible thing,” she thought. “I paid it off completely. Why is the system punishing me for doing what I was supposed to do?”

If this moment sounds painfully familiar, you’re far from alone. Thousands of people experience this exact emotional whiplash every single month.

Here’s what actually happened in Sarah’s case — and what usually happens in yours.

At that point, most people don’t just want an explanation — they want to actually see what changed. That’s where tools like SmartCredit and myScoreIQ (Affiliate Disclosure) can be helpful, because they allow you to actually see your score changes as they happen — not days or weeks later when you’re left guessing what changed.

In other words, your score reacts to signals — not intentions. And once you understand that, everything else about credit starts to make a lot more sense.

This idea is explained in more detail in the credit scoring models framework, where the system behind how scores are calculated becomes much clearer.

If we strip this down to its simplest form, here’s what actually happened:

When you step back and look at it from the system’s perspective, the pattern becomes much clearer:

Pattern Snapshot

Action: Credit card balance paid off to zero

System Interpretation: Sudden shift in utilization and account activity signals

Score Impact: Temporary fluctuation or small drop as the model reassesses risk

Timeline: Immediate adjustment, then stabilization over 1–6 months

The system doesn’t see “good decision” or “bad decision.” It sees patterns. When Sarah’s balance dropped dramatically to zero, the scoring models registered a sharp change in the signals they had been tracking — especially around how much credit she was actively using and how her account behavior looked overall.

This is what we call the Utilization Reset Effect. In simple terms, this just means the system is reacting to how your balance suddenly changed.

This connects directly to how utilization is interpreted in scoring models, which is covered more deeply in the credit utilization and credit card behavior framework.

This is the moment where most people pause and realize something important: nothing actually went wrong. What felt like a setback was just the system adjusting to a new signal.

This adjustment doesn’t happen all at once — it unfolds in stages. And this is where most of the confusion comes from — because you’re seeing one moment, while the system is looking at a longer pattern.

Timeline of What Typically Happens

0–30 days: The score reacts to the updated zero balance reported by the creditor.

1–3 months: The model begins adjusting as new usage patterns (or inactivity) start to appear.

3–6 months: Things typically stabilize as the system gets used to the new normal.

6+ months: A longer-term pattern becomes established.

This is also why people who actively track their credit tend to understand it much faster. Instead of guessing, they can actually see these stages play out in real time. Platforms like SmartCredit and myScoreIQ (Affiliate Disclosure) allow you to follow your score changes month to month, which is often the point where everything finally starts to click.

This timeline effect is something that shows up across multiple areas of credit scoring, including how payment patterns are interpreted over time in the payment history and delinquency patterns framework.

The way this plays out can look a little different depending on what changed in your situation:

If you paid off just one card, the signal shift is often small and the drop may be minor or even unnoticeable.

If you paid off several cards at once, the pattern change can be larger and the temporary fluctuation more noticeable.

If you pay off the card and then stop using it entirely, the reduced activity can create a different kind of signal over time.

These types of shifts are also influenced by how long your accounts have been active, which is part of what’s explored in the credit age and file depth framework.

Expectation vs System Reality What most people expect: “Paying off debt should immediately boost my score.” What actually happens: The system reinterprets your entire profile based on the updated signals. A sudden zero balance can temporarily shift the calculation before new patterns form.

Frequently Asked Questions

Why does it feel like I’m being punished for doing the right thing? Because the system isn’t evaluating your decision the way you are. It’s responding to how your credit profile changed, not why it changed.

Why did my credit score drop after paying off my credit card? Because the system detected a shift in utilization and activity signals, not because of the positive action itself.

Is this drop permanent? No. It is usually temporary and stabilizes as new patterns form over 1–6 months.

Should I be worried? In most cases, no. This is a normal pattern adjustment many people experience.

How long does it take to recover? Typically 30–90 days, depending on reporting cycles and your ongoing credit behavior.

If you want to stop guessing and actually understand how your score responds to changes like this, using a credit monitoring tool is often the simplest way to connect the dots. Being able to see your data update in real time turns confusion into clarity — and that’s when everything starts to click.

And once you can see those patterns happening, it’s much easier to stop worrying about every small change.

If you really want to understand why these changes happen, it helps to see how all of these factors work together — from utilization to account age to overall scoring models — which is exactly what the full Credit Patterns framework is designed to explain.

Credit scores don’t react randomly — they follow predictable patterns. Once you understand the pattern, what used to feel confusing and even unfair starts to feel logical.

The next time you see an unexpected change after doing the “right thing,” you’ll know it’s not a punishment. It’s simply the system recalibrating to new signals. And once you see it that way, what used to feel frustrating and even unfair starts to feel predictable.

Written by the CreditPatterns.com Education Team — Focused on explaining credit system patterns in clear, neutral language. Disclosure