Follow the Credit System Step-by-Step

How Payment History Shapes Your Credit Score

Payment history is a key factor in credit scoring models, reflecting your track record of on-time or late payments and its impact on your overall credit health.

5/8/20245 min read

Payment history is the most influential factor in how credit scores are calculated — yet it’s also one of the most misunderstood.

Many people assume credit scores are affected by a few isolated actions, like making a payment on time or missing one by accident.

But in reality:

👉 Payment history is not about individual events

👉 It is about patterns that are built, recorded, and interpreted over time

Understanding how this pattern works is the key to understanding how credit scores are actually calculated.

A Scenario You’ll Probably Recognize

You’ve made most of your payments on time.

But your score still isn’t where you expect it to be.

Or:

A single missed payment caused a noticeable drop.

That leads to the question:

👉 Why does one part of your credit profile carry so much weight?

The Core Role of Payment History in Scoring Models

Payment history reflects:

whether payments were made on time

how often delays occur

how recent those delays are

how severe the delays become

These patterns are evaluated within the broader system described in the Credit Scoring Models Framework, where different models interpret reported data using statistical relationships rather than individual intent.

Payment History Is Built on Reported Data — Not Behavior

One of the most important concepts to understand is this:

👉 Credit scoring models do not see your actions

👉 They only see what is reported

Payment history exists because of how data is structured and transmitted through the system, as explained in the Credit Data Reporting & Structure Framework.

That means:

A payment is only reflected when it is reported

Timing determines how it appears

The structure of the data determines how it is interpreted

How Payment History Is Actually Recorded

Payment history is not a single data point.

It is a structured timeline that includes:

monthly payment status

account condition (current, late, delinquent)

severity of delays (30, 60, 90+ days)

charge-offs or collections

These elements form a pattern that is continuously evaluated as part of your credit profile.

Why Payment History Carries the Most Weight

In most scoring models:

Payment history represents the largest category

It is strongly associated with long-term risk patterns

It reflects consistency over time

But this doesn’t mean one late payment defines everything.

👉 It means the pattern matters more than the moment

This distinction is critical, because credit scoring models are designed to evaluate behavior over time rather than isolated actions.

🔍 What Is Payment History in a Credit Score?

Payment history is the record of on-time and late payments reported by creditors, forming a structured timeline that credit scoring models use to evaluate patterns of behavior over time.

🔍 Why Is Payment History So Important?

Payment history carries the most weight because it reflects consistency and reliability over time, which are strongly associated with how risk is modeled in credit scoring systems.

🔍 Can One Late Payment Affect Your Credit Score?

Yes. A single late payment introduces a new negative data point that can change how your entire credit profile is interpreted, especially if it is recent.

The Importance of Time and Recency

Payment history is not static.

It evolves based on:

how recent a missed payment is

how frequently issues occur

how long positive history continues afterward

This is part of how scores change over time, which is explained in the Credit Score Changes & Fluctuations Framework.

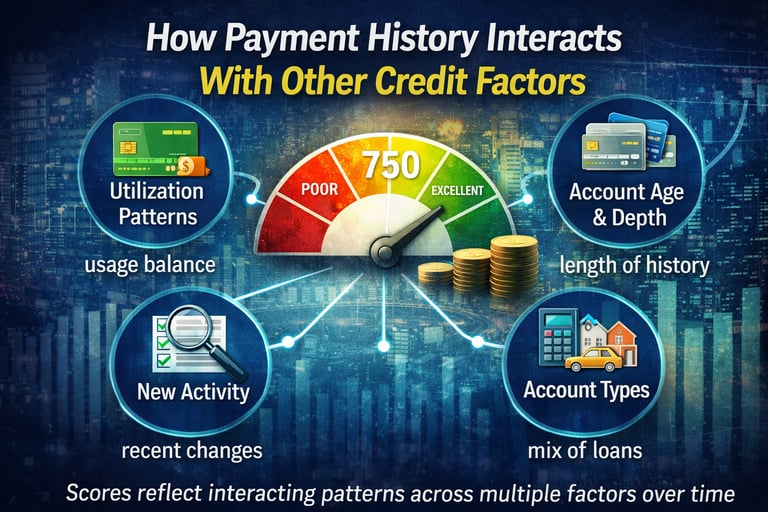

How Payment History Interacts With Other Factors

Payment history does not exist in isolation.

It interacts with:

utilization patterns (Credit Utilization & Credit Card Behavior)

account age and depth (Credit Age & File Depth)

account types (Credit Mix & Account Types)

new activity (Credit Inquiries & New Credit Activity)

👉 Scores are not driven by one factor

👉 They are driven by interacting patterns across multiple factors over time

Why a Single Late Payment Can Have a Big Impact

A missed payment introduces a new data point into the system.

That data point is:

recent

structured as negative

interpreted within existing patterns

Because scoring models prioritize patterns associated with risk, even one new event can shift how the entire profile is interpreted.

Why Payment History Feels Unforgiving

Many people feel like:

👉 “I made one mistake — why does it matter so much?”

The reason is:

👉 Scoring models are pattern-based systems

They don’t evaluate:

intent

circumstances

effort

They evaluate:

👉 reported data and statistical relationships

The Role of Reporting Cycles

Timing plays a critical role in how payment history appears.

Because data is reported in cycles:

a payment may appear late depending on timing

updates may not reflect immediately

different bureaus may show different snapshots

This connects back to how credit data flows through the system in the Credit Data Reporting & Structure Framework.

Why Payment History May Look Different Across Reports

You may notice differences across platforms.

This happens because:

not all lenders report to all bureaus

updates occur at different times

models interpret data differently

Which is why scores can vary, as explained in:

👉 Why Your Credit Score Is Different on Every App

Observing Payment History Over Time

Some individuals choose to observe how their payment history appears and changes over time using monitoring services.

These platforms provide visibility into:

how payment status is reported

how updates appear across reporting cycles

how score changes correspond to those updates

This allows users to see how payment patterns are reflected within scoring models rather than relying on a single moment in time.

👉 For a deeper explanation of how payment activity appears across reporting cycles, see the Credit Monitoring & Credit Tools Framework, where scoring systems interpret patterns of reported data.

Common Observable Patterns in Payment History

Across many credit profiles, patterns often include:

consistent on-time payments associated with stronger scores

recent late payments associated with noticeable changes

older negative items having reduced impact over time

multiple late payments amplifying impact

These are patterns observed within data — not guarantees.

How Payment History Fits Into the Full System

Payment history is one component of a larger system.

That system includes:

how data is reported (Credit Data Reporting & Structure)

how models interpret it (Credit Scoring Models)

how changes occur over time (Credit Score Changes & Fluctuations)

👉 Understanding your score requires understanding all three

Key Takeaway

Payment history is not just about whether you paid on time.

It is:

👉 a structured pattern of reported behavior over time

That pattern is interpreted by scoring models, influenced by timing, and shaped by how it interacts with other parts of your credit profile.

Frequently Asked Questions

How important is payment history in a credit score?

It is typically the largest factor in most scoring models, reflecting patterns of payment behavior over time.

Does one missed payment ruin your credit?

It introduces a new data point that may affect how your profile is interpreted, especially if it is recent.

How long do late payments stay on a credit report?

They may remain for several years, but their impact may change over time depending on recency and surrounding data.

Why did my score drop after a late payment?

Because scoring models interpret new negative data within the context of your overall credit profile.

Does payment history affect all scoring models the same way?

No — different models may weigh and interpret payment history differently, as explained in the Credit Scoring Models Framework.

🔗 Explore the Credit Education Framework

To understand how payment history fits into the bigger picture:

Each section explains one component of how credit scoring models interpret real-world credit data.